GreenStone Farm Credit Services is proud to announce the recipients of both the GreenStone Scholarship and the Dave Armstrong Scholarship in 2025, totaling $60,000 in educational support awarded to exceptional students. Since 2010, GreenStone has awarded more than $500,000 in scholarships to students preparing to make a positive impact in the agriculture industry.

The GreenStone Scholarship Program selected 21 high school seniors who demonstrated outstanding dedication to coursework, extracurricular activities, leadership, and a strong commitment to pursuing careers in agriculture. Recipients received either a $2,000 or $1,000 award to support their education.

The 2025 awardees for the GreenStone Scholarship are: Allie Choate (Cement City, Mich.), Ava Totzke (Stevensville, Mich.), Blake Jauquet (Luxemburg, Wis.), Bryce Ritter (Byron, Mich.), Carter Lenzer (Valders, Wis.), Celina Eldridge (Stanton, Mich.), Chesaney Wenzlaff (Kingston, Mich.), Colby Tucker (Hopkins, Mich.), Darek and David Trzebiatowski (Waupaca, Wis.), Elayna Hawkins (Freeport, Mich.), Elizabeth Hartmann (Flint, Mich.), Jacob Rohm (Seymour, Wis.), Kaden Petroshus (Gobles, Mich.), Madison Wiese (Greenleaf, Wis.), McKenzie Voisinet (Laingsburg, Mich.), Owen Epple (Watervliet, Mich.), Owen Newland (Belding, Mich.), Patrick Priesman (Bellevue, Mich.), Rylee Nelson (Waupaca, Wis.), and Sydney DuRussel (Reese, Mich.).

In addition, four outstanding college students were awarded the Dave Armstrong Scholarship, named after GreenStone’s former CEO, who dedicated 41 years at GreenStone, advancing agricultural innovation and stewardship. This prestigious scholarship, $5,000 each, aims to recognize and support students continuing to pursue careers in agriculture, timber, and natural resources.

The 2025 awardees for the Dave Armstrong Scholarship are: Abigail Guza (Ubly, Mich.), Jenna Gries (Manitowoc, Wis.), Laken DuRussel (Munger, Mich.), and Lily Mendels (Holland, Mich.).

“At GreenStone, we have a deep commitment to investing in the future of agriculture by empowering the next generation of leaders,” said Travis Jones, President and CEO. “By providing financial support to these students, we aim to enable them to pursue their dreams and inspire a bright future in agriculture across Michigan and northeast Wisconsin.”

Each student selected for either of GreenStone’s scholarships met specific criteria, including residency within GreenStone’s territory, competitive GPA, and plans to pursue an agriculture or natural resources-related field. Additionally, awardees demonstrated active community involvement, leadership in school and a passion for agriculture.

Applications for the 2026 scholarships will be available on the GreenStone website in early 2026, providing another opportunity for aspiring agricultural leaders to apply for financial support.

While running his agricultural business and getting his Crop and Soil Science degree in Oklahoma, Logan Maher learned the value of partnering with Farm Credit after working with them on various projects. So, when he moved up to Michigan there was no hesitation when reaching out to GreenStone.

As newlyweds, Logan and Jenna Maher bought their first piece of land in April of 2024, consisting of 115 acres. Although not all of the acreage was tillable, the couple planned to utilize various methods to get the land exactly how they wanted!

Having sold his business in Oklahoma when he moved to Michigan, Logan faced an unexpected tax burden and noted, “I definitely learned my lesson from that and decided that planning is a pretty critical thing to do while running a business.”

This meant when starting fresh here in Michigan, he wanted to ensure his new operation was set up for success. That’s when he reached out about GreenStone’s CultivateGrowth grant. Logan utilized the grant to work with a business planning agency he trusted to make sure he and Jenna were on the right track.

The Mahers both come from strong agricultural backgrounds and currently operate the farm while working full-time off the farm. The tillable land houses a cucumber crop for this summer, and the Mahers plan to build a steady rotation in the future. GreenStone also helped them close on an equipment loan to purchase an excavator, so they can further clear their land and assist others in the surrounding area. Their goal is to get as much of their land fully tillable to allow them to increase the size of their crop.

With the couple’s dedication to their success and support of GreenStone, the Mahers are excited for their future on their land.

GreenStone aims to provide opportunities for all young, beginning, and small farmers and supports their educational and personal growth efforts with our CultivateGrowth grant. To learn more about GreenStone’s CultivateGrowth grant, click here.

Pictured above from left to right: Bruce Lewis, Michael Feight, Rick Snyder, and Paul Lindow.

Two current board members have been re-elected to the GreenStone Farm Credit Services Board of Directors: Michael Feight and Bruce Lewis.

Michael Feight of Lenawee County, Michigan, was reelected to a four-year term representing voting region 3, located in the seven counties covering the southeastern corner of Michigan. Feight farms corn, beans, and wheat alongside his father and brother on their family farm. He has served on the GreenStone board for the past four years, and most recently as a member of the Finance Committee.

Bruce Lewis of Hillsdale County, Michigan, was also reelected for another four-year term representing voting region 3. Lewis, a livestock and grain farmer, has served on the board since 2011 and most recently was a member of the Audit Committee.

GreenStone’s board of directors have also selected two new appointed directors to serve on the board: Paul Lindow and Rick Snyder. As a financial expert, Lindow will chair the board’s Audit Committee, while Snyder brings his expertise in technology and cyber security with him to the board and will chair a new, soon to be established Technology Board Committee.

“As a member-owned cooperative governed by our members, GreenStone recognizes that when our members are successful, so are we,” said Travis Jones, GreenStone President and CEO. “The re-election and appointment of these board members demonstrates their deep understanding of the values and needs of our cooperative. They have consistently shown their leadership and dedication to our mission of strengthening the rural communities we serve in Michigan and northeast Wisconsin.”

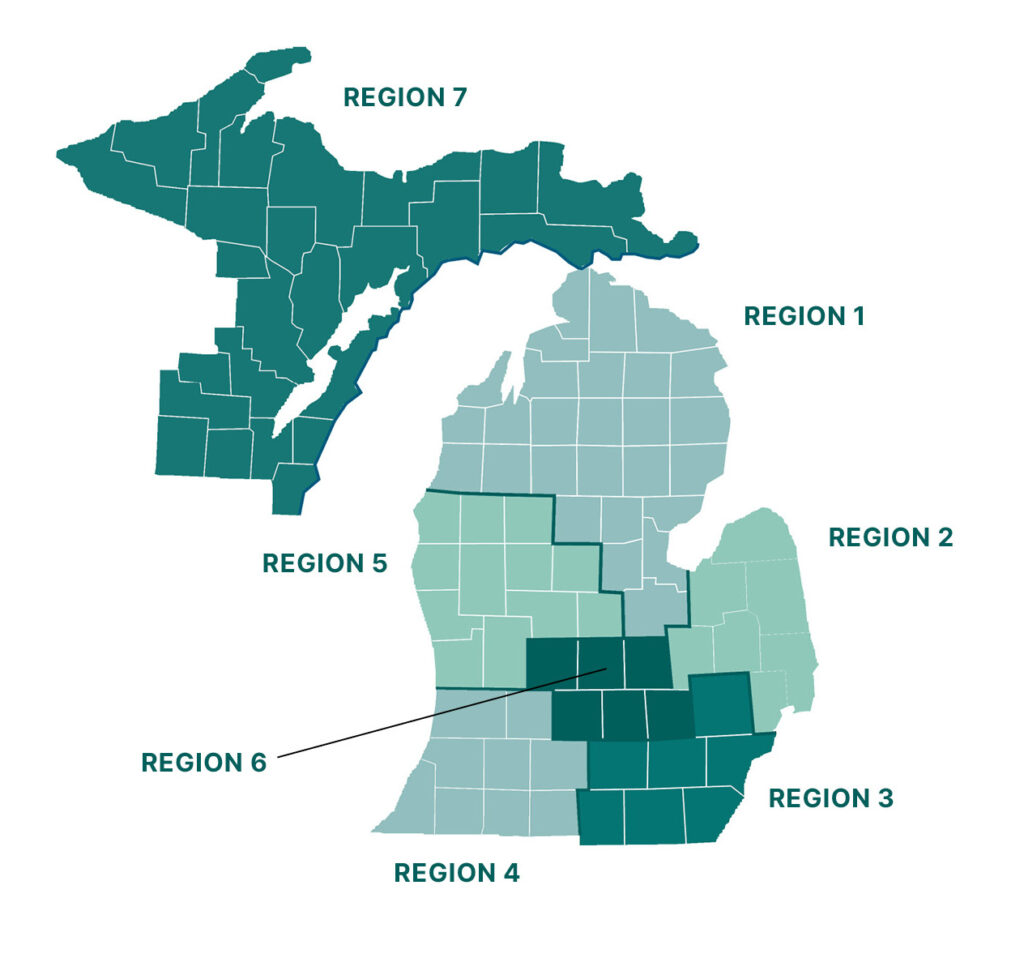

Along with the board positions, GreenStone’s 28,000 members elected individuals to serve on the cooperative’s 2026 nominating committee. The nominating committee is comprised of GreenStone members from throughout the organization’s territory who are tasked with recruiting candidates for next year’s board elections and nominating committee. The 2026 nominating committee includes:

Region 1 – Nathan Clarke (Midland County, MI), and Deidre Iciek (Gladwin County MI)

Region 2 – Ty Bodeis (Tuscola County, MI), and Grant Davidson (Sanilac County, MI)

Region 3 – Calby Garrison (Lenawee County, MI), and Jason Winter (Monroe County, MI)

Region 4 – Joseph Dykhuis (Allegan County, MI), Scott Hassle (Van Buren County, MI), and Benjamin S. Schilling (Berrien County, MI)

Region 5 – Michelle L. Nitengale (Montcalm County, MI), Ann M. Patin (Newaygo County, MI), and Tyler Wilson (Gratiot County, MI)

Region 6 – Damien Miller (Shiawassee County, MI) and Francis Trierweiler (Clinton County, MI)

Region 7 – Johna C. Brock (Oconto County, WI) and Kim Kinjerski (Kewaunee County, WI)

Getting Involved in Your Cooperative

As a member of GreenStone, you play a crucial role in determining the governance and leadership of our association! Make your voice heard by participating in elections and consider getting involved by submitting your interest in a nominating or director role.

Members from GreenStone’s voting regions 4 and 5 will gather in August to find candidates for open director and nominating committee positions for 2026’s elections. The remaining regions will meet in December to choose candidates for their nominating committee positions. This is your opportunity to take an active role in your cooperative’s future. We encourage you to consider participating in the governance process and submit your interest today!

The Importance of the Nominating Committee

Before a member can be elected to the board, our Nominating Committee identifies, evaluates, and nominates a qualified slate of candidates for stockholder election. The Nominating Committee holds a very pivotal role in determining who provides leadership to our association.

If you’re interested in furthering GreenStone’s role as an industry leader for agriculture and our rural communities, serving on the Nominating Committee might be a great opportunity for you!

Get Involved Today!

To learn more about the nominating and director roles, visit greenstonefcs.com/about-us/board-of-directors/governance-overview/. Complete a profile to express your interest or contact our corporate governance coordinator, Cheryl Motz at [email protected] or 517-318-9557, for more information.

As a young, beginning, or small farmer, how can you position yourself for success when seeking to work with a lender to grow your farming operation? The Five Cs of Credit are a steppingstone to get you there! Dive into what each of these “Cs” mean, and how a better understanding of each of them can help you along the way as you grow your business.

Character

The more information you can provide to your lender up front about yourself and your business, the better! Share with your lender who you are, your background, and what your business goals and aspirations are. Even if you don’t have every detail of your business plan worked out, sharing as much as you can about your goals for your business will go a long way in helping your lender get to know you.

Inviting your financial services officer to your farm is a great opportunity for them to learn more about you and your business. It will help strengthen your relationship with your lender.

Capital

Capital gives your lender a snapshot of your personal financial statement, better known as a balance sheet. A balance sheet is a list of all your assets and liabilities — what you currently own and what you owe on. If you don’t have a balance sheet completed, don’t hesitate to ask your financial services officer to walk you through filling it out. We’re here as a resource and would be more than happy to assist you in learning how to complete it.

Your lender will also evaluate if you have more assets than liabilities. If not, it is important to communicate with your lender what your debt management strategy is going forward.

Capacity

Your ability and plan to repay debt is your capacity. This can include any existing debt as well as any new debt you are planning on taking on. Providing your lender with your plan for managing your debt will go a long way. If you can provide projections for multiple scenarios to your lender on your debt repayment plan, that is even better.

This will help them get an idea of your management abilities and show them you are willing to go the extra mile to provide the most information possible to your lender. Again, the more information you can provide up front, the smoother the lending process will be, the stronger the relationship will be with your lender, and the more your lender will be able to support you!

Collateral

Collateral acts as a secondary source of repayment and is required with every loan you are applying for with GreenStone. If you do not have a lot of assets that could be used as collateral for your loan, it will be important to have a cash down payment up front. The more you can put down as a down payment, the less you will have to use as collateral.

It’s important to remember that any collateral you use towards your loan must be a tangible asset and have some relation to your loan. For example, if you are taking out a loan for a new piece of equipment, you might be able to use equipment you already own as collateral.

Conditions

Conditions are the terms of your loan that keep both you and your lender accountable to each other. A condition of your loan may be that your lender requires a balance sheet every year throughout the length of the loan to monitor the progress you’ve made and to make sure you are on track for full loan repayment. Think of it as a way to check in with your lender and keep an open line of communication. We want to know how we can continue to best support you!

The Five Cs of credit are a framework meant to work together to present a full picture of yourself and your business plan to your lender so they can assess a loan solution that works best for you. Understanding each and why they are important will prepare you for conversations with your lender about the plans you have to grow your business. Your local GreenStone branch is available to answer any questions you might have on the Five Cs of Credit or what your lender is looking for when applying for a loan.

This article was originally published in Michigan Farm News.

Do you dream of wide-open spaces, away from the hustle and bustle of the busy city? Do you envision looking up and seeing the stars at night? Are you ready for a slower-paced life on your own land, living the country life you’ve always imagined? There are plenty of great reasons to move out to the country, but here are five more that might just convince you to take the next step and embrace the rural way of life!

1. Land values continue to rise

You’ve probably heard the saying “They’re not making any more land” when referring to the increasing value of land prices, and there is a lot of truth to it. Land prices have continued to steadily increase. In some areas land prices have doubled in the last five years. As more and more people embrace rural living and are moving out to the country, the upward trend for land values is likely to continue.

Think of your new rural home or property as an investment in your future. Mid to large size parcels ranging from 10-50 acres have continued to rise in popularity due to people seeking to live more independent and self-sufficient lifestyles. The demand for more space and a more flexible way of living isn’t going away. While that saying may seem like a cliché, there is something to be said about owning something that truly is a limited resource!

2. Lower cost of living

Rural living has more benefits than just being out in the country. The cost of living is often lower in less populated areas. Property taxes, land costs, and many living expenses are often lower in the country.

Living outside of city limits also allows you the opportunity to use alternative heating and cooling methods. For example, you could choose to heat your home with a wood stove and harvest firewood from your own property.

If you live in town, municipalities control the cost of utilities, such as water. Living in the country allows you more control over these costs. While the upfront cost of installing a well and septic system for your home can be a larger investment, there are no ongoing monthly costs, likely saving you more money on utilities in the long run.

3. Opportunities for alternative sources of income

Living on your own property provides the opportunity to use your land as a source of income through, for example, part-time farming. Not only does having your own land present you with an opportunity to become more self-sufficient and feed your own family, but it also can help provide income for your family too.

If you’re dreaming of starting your own vegetable garden, consider getting a chicken coop so you can have your own eggs, or planting a cut flower garden. Roadside farm stands are a popular way to turn one of your hobbies into an alternative source of income that wouldn’t be possible in a town or city context.

4. More access to nature and recreational hobbies

One of the biggest reasons people plant roots in the country is to experience a slower pace of life. That doesn’t mean there aren’t plenty of exciting aspects of country living! Living in the country can mean easy access to the great outdoors and a number of recreational hobbies such as hiking, kayaking, fishing, hunting, biking, camping, and just spending plenty of time outdoors.

Stop to watch the sunset and get a clear view of the stars away from the lights of the city. Take advantage of the natural beauty and wildlife that surrounds you. If you value more space, more privacy, and more access to nature, then rural living could be ideal for you.

5. Close-knit communities

There’s nothing like getting to know your next-door neighbor, even if they live a mile down a dirt road! Living in the country, or a small town or village, has many benefits including generally closer-knit communities, and of course that homey small-town feel. Many families also choose to move to rural areas because of smaller school districts and classroom sizes for more opportunities for hands-on learning.

Moving to the country can also give you a newfound appreciation for the farming and agriculture around you as you watch the seasons change with your local farmers from planting time all the way into harvest season.

There are endless reasons to move out to the country and embrace a more rural lifestyle. No matter what reason you have for making the move, you are bound to experience even more benefits than you would have thought the longer you find yourself living in the country!

Contact your local GreenStone branch to learn more about rural home and vacant land financing options.

Vacant land, home site and recreational property loans have become especially popular over the last few years as families look for ways to get out and enjoy nature.

Summer is here. As you’re spending more time outdoors, you might be considering if now is the time to invest in a property to begin making memories on. Whether you’re interested in building your dream home on vacant land or owning recreational property, GreenStone can help you finance property that fits your budget and supports your plans for the future.

Which land loan is the best fit for me?

There are many things to consider when deciding what kind of land loan will fit your needs best. It’s important to understand the characteristics of each loan, beginning with the type of property being financed and your long-term goals.

What’s a recreational land loan?

Recreational land with GreenStone is defined as more than five acres being used primarily for recreational purposes. A recreational land loan typically requires a 20% down payment, but in some cases it could be as low as 15%. GreenStone offers 30-year amortization terms for affordable payments. This land is usually used for hunting, fishing, hiking or ATV-riding, with no immediate plans for building at the time of purchase. If you have interest in building a home, pole barn or outbuilding later, GreenStone can provide do-it-yourself or contracted construction loans to fit your needs.

How does a vacant land loan work?

Similar to recreational land, vacant land is often property that is greater than five acres. What’s the difference? This property is purchased with the intention of building a structure on it. The terms of vacant land loans are like recreational land loans as a typical down payment is 20%, with some cases allowing a 15% down payment.

What defines a home site loan?

A home site property financed with GreenStone is commonly land that is less than 5 acres and does not have any structures on it. These loans are typically used by customers who plan to build a home or cabin on the land. Financing options vary for each individual and property type. However, the requirement is usually 20% down, with certain instances allowing you to put down as little as 15% down with a 30-year term.

Recreational Land FAQs

What are my down payment options?

As mentioned above, recreational vacant land mortgages typically require a 15-20% loan to value down payment. GreenStone has options for borrowers looking to secure their down payment, including:

- Providing 20% cash down.

- Other property or forms of collateral to meet some or all the down payment requirements.

How do I reamortize my loan?

Loan reamortization, referred to as an interest rate loan conversion, can be done quickly without the need to refinance throughout the life of the loan as equity is accumulated. A visit with a local GreenStone financial services officer can get the process started.

Can I finance vacant land for up to 30 years?

Yes, GreenStone is one of the few lenders who will write mortgages on land without the stipulation to build within a certain timeframe. Many of our customers use our land mortgages to purchase hunting land or recreational land.

Many people are taking advantage of GreenStone’s flexible financing to purchase property not just for today, but for a place they will keep in their family for generations to come. To learn more about home site loans, recreational land loans, country home mortgage loans and finding the best loan for your needs, visit a GreenStone branch near you.

The United States dairy industry is both bullish and bearish for producers, with many factors potentially influencing the future.

While export demand and record-high processing investment offers momentum, policy uncertainty – spanning labor, trade and nutrition assistance – combined with soft domestic demand has created downward pressure.

Milk prices are seemingly carrying over from last year with strong milk prices in the first quarter. Growers are also experiencing lower feed costs. However, tariff discussions recently caused some volatility in the futures markets, especially for Class III (cheese) prices.

“There’s always volatility in our industry, but cheese prices have rebounded and are currently profitable, with futures indicating sustained profitability for the next 6-12 months,” says Mitchell Schafer, vice president of agribusiness lending at GreenStone Farm Credit Services. “It’s no longer just, ‘what’s my local milk price?’” he says. “Some of the rebound in milk prices came from the export market, where the U.S. has competitive prices in the global cheese market. Retaliatory tariffs remain a concern.”

The U.S. dairy market is heavily influenced by international competitiveness, with approximately 16% of milk solids currently being exported, according to Leonard Polzin, Dairy Markets and Policy Outreach Specialist at the University of Wisconsin-Madison Extension.

High dairy market prices have been historically influenced by either reduced production or increased exports. As the industry looks towards the future, maintaining competitive pricing on the world stage will be crucial for sustaining strong margins, Polzin says. The U.S. exports nearly one-fifth of dairy components, primarily nonfat solids, with Mexico, Canada and China collectively accounting for about 40% of the total value of U.S. dairy exports in 2024, according to Polzin.

Investment in Processing Infrastructure

Capital costs and interest rates are higher than they were four years ago, posing challenges for growth, according to Schafer. However, there is expansion, as the U.S. dairy industry is experiencing substantial investment in processing infrastructure, exceeding $8 billion nationwide, with some estimates approaching $9 billion. Notable projects include:

- Walmart’s $350 million facility in Robinson, Texas, expected to be operational by 2026

- Fairlife’s $650 million fluid milk plant in New York

- Chobani LLC’s recently announced $1.2 billion dairy processing facility, which broke ground on April 22 in Rome, New York

This surge in milk processing is expected to create a higher demand for milk and could lead to a more stable and profitable market for dairy farmers. The price bump may stretch out depending on how long it takes for farmers to align production.

Much of the new processing investments are concentrated in cheese production. U.S. cheese exports have outperformed expectations due to lower prices relative to the European Union, where tight milk supplies have driven prices higher. This price gap has made U.S. products more competitive, but the advantage is fragile, according to Polzin.

Milk Solids Production Continues to Increase

Despite a 0.35% year-to-date decline in total milk production in 2025, calculated milk solids production increased by 1.65% as of March 2025. This increase in production efficiency coupled with an increase in the national herd of 15,000 head from January to March of 2025 and an increase of 57,000 head year-on-year, means the industry can meet new demand for milk solids more quickly than in the past, according to Polzin.

High oleic soybeans are gaining traction for increasing butterfat and protein content in milk. “It depends on production levels as to the response growers might see,” Schafer says. “There are herds that are running trials, and some are making that switch, but it’s not cheap to put in a roaster, grinder and storage to handle it. Sourcing or growing the beans yourself can also pose challenges. Producers in the 80-pound to 90-pound range may see bumps in the components (butterfat and protein) and production, as well.”

Dairy Replacement Values Remain High

“It can be expensive to buy cows. That goes for calves, heifers and springers,” Schafer notes. “But at the same time, producers are getting pretty good money if they’re selling cull cows, or day-old black calves – at least they’ve gone up together,” he says.

Dairy replacement values are high. In April, USDA reported the average price for a dairy herd replacement ready to enter the milk barn reached $2,870. That’s up from $2,120 the same time last year.

In the final 18 weeks of 2023, dairy farmers sent 140,500 fewer dairy cows to slaughter when compared to the previous year. The big pullback continued throughout 2024, as 367,400 fewer head of dairy cows went to slaughter as dairy farmers looked to shore up herd numbers when faced with fewer heifers, according to Corey Geiger, lead dairy economist at CoBank.

That trend seems to finally be reversing. Through March, the U.S. dairy cow herd was up 80,000 head when compared to the start of 2024. However, that gain, which reached a total of 9.4 million head, has less to do with replacement inventories and more to do with a historic pullback in culling, which started in the fall of 2023.

“Some producers are getting another lactation or two lactations out of their herds,” Schafer says. “Instead of culling they are getting more milk out of them because the price is favorable right now, and because there aren’t as many replacements out there.”

Butterfat Exports Rising in 2025

Butterfat exports were 203% higher than a year ago in March at 17.9 million pounds, according to the U.S. Dairy Export Council. Canada was a major buyer as sales volume grew 172% compared to the same time last year.

“Overall, U.S. butter prices continue to be discounted compared to the two largest global dairy exporters — the E.U. and New Zealand,” Geiger explains.

While March 2024 still holds the record of 110 million pounds of cheese exported in one month, March 2025 secured the number 2 spot at 109 million pounds. Mexico remains the top U.S. dairy customer and purchased 95.5 million pounds of cheese in the first quarter of 2025.

“It was a clean slate, I could do whatever I wanted with the land which was really nice,” Gregory Lewandowski recalled after he bought land from his grandparents in 2018. Just after that land purchase, he was deployed with the National Guard in Afghanistan. He spent much of his free time researching the best methods to farm his land and how he could accomplish his goals from the ground up.

While deployed, Gregory said he found GreenStone when he had to file farm taxes for the first time. “My Dad went into the office on my behalf to present my information and they did all the legwork on my taxes after we just showed up as a stranger on their doorstep. I appreciated that and stuck with them.”

Returning to his farm, Gregory’s research helped him land on direct-to-consumer grass-fed beef. He focuses on using rotational grazing and regenerative pasture management to see the best results in his cattle and soil integrity. He noted, “At its core, regenerative agriculture is simply farming in harmony with nature, not fighting it.” Since developing his operation, he now grazes his cattle over three different properties and 180 acres.

To continue his passion for learning, Gregory enrolled in a six-year rotational course through Northeast Wisconsin Technical College. With GreenStone’s CultivateGrowth grant he was able to reimburse a portion of his course fee. The course topics vary from year to year and cover new ideas from soil management, agronomy, animal nutrition, and farm financials. “As we know with farming, like any industry, it’s consistently changing. So, there are new ideas they present, and you may have never considered them.”

While staying up to date on new methods is educationally great, he noted the best thing the course provided was communication and networking with other farmers. He said he had a great group of classmates and has since worked with multiple people on various projects around his farm. He laughed, “In fact, someone I met in class came and rescued me off the highway when I had a flat and a trailer full of cattle.” Whether on the road or in the classroom, Gregory has built a supportive community to help him reach his goals.

GreenStone is proud to be a part of Gregory’s community. We’ve got him covered from tax preparation to educational opportunities. GreenStone aims to provide opportunities for all young, beginning, and small farmers and support their educational and personal growth efforts with our CultivateGrowth grant. To learn more about GreenStone’s CultivateGrowth grant, click here.

When you’re just getting started as a beginner farmer, it’s easy to feel overwhelmed by the amount of new information you’re learning and keeping track of everything you need to stay organized and successful. Whether you are in line to take over operations of your family’s multi-generational farm or starting your own farm from the ground up, here are some questions to consider ahead of meeting with your lender to help them provide you with the best support possible!

1. Define your business goals

The first step in any business should always be to define your goals. Not only will this help to inform the decisions you are making around your business, but it will also set you up for success when it comes to working with your lender to help them clearly see your vision and strategy for your business. A clear and defined business strategy acts as a roadmap for achieving your goals.

Start by defining your SMART goals – that means specific, measurable, achievable, relevant, and time-bound goals. This framework will help you prioritize which goals are the most important and help you dive deeper into the details of your vision for your farm. Understanding your needs ahead of time is crucial to effectively communicating with your lender and developing a plan that fits your needs the best.

Before engaging with your lender, take the time to thoroughly assess your business strategy and financial goals. Having a clear vision of your lending requirements, including specific purposes and estimated costs, is essential. This preparation will not only streamline your conversation but also position you as a well-informed borrower.

2. Provide as much information up front to your lender as possible

Even if you don’t have every detail of your business plan worked out or your balance sheet filled in, providing as much information as you possibly can will go a long way in helping your lender determine what your needs are. Your local GreenStone team has been helping farmers like you for over a century and would be happy to sit down with you to review how to complete these important financial documents.

Another reason it is important to provide as much information as possible to your lender is to help them match your loan terms to your specific needs. Let’s say you are looking to finance a piece of farm equipment such as a tractor. You will want to opt for a short-term loan request versus a long-term request for something like a land purchase.

If you know you will need financing for farm equipment in addition to a construction loan for adding on to your facilities, it is important to communicate this to your lender as soon as possible. They may be able to package your lending needs together into one loan request. This is yet another reason why it is important to provide as much information to your lender up front as you can!

3. There are resources available to help you!

While it may feel daunting when you are first starting out, there are a multitude of resources available to you as a young, beginning, or small farmer. Many organizations like Farm Bureau and other members of the agricultural industry offer educational and networking opportunities or resources valuable to you. GreenStone’s own CultivateGrowth program offers a mentorship, educational resources, grants, and more to support up and coming farmers whether you are starting your own farm or taking the reins of a multi-generational farm.

Many agricultural lenders also offer more relaxed underwriting standards to help beginning farmers overcome the financial challenges they might face being a new farmer to help them get started.

When you work with an agricultural-based lender, not only are you able to receive financing and support specific to your growing farm, but chances are you’re also getting the expertise of fellow farmers. Many members of our team at GreenStone are involved in running a family farm, have a hobby farm or farm animals, or are involved in supporting a number of agricultural organizations outside of work. At GreenStone, we live the country lifestyle too! Having a lender that knows what you’re experiencing – because we’ve been there too – is paramount to the kind of support you will receive when you are first starting out as a beginning farmer.

If you have any questions on resources for beginning farmers or are ready to take the next step and apply for financing for your farm, reach out to your local GreenStone expert. We are eager to support the next generation of young, beginning, and small farmers.

This article was originally published in Michigan Farm News.

“Were you raised in a barn?” may have been a popular sarcastic comment in the past but today, growing up in a barn is a very desirable option to many people! Barn homes, also known as barndominiums and barndos, continue to gain popularity across the country. Barn homes can offer soaring ceilings with unique wide-open living spaces, speedier exterior construction and other attractive options. Functionally, the potential to combine work and living spaces or storage for recreational vehicles in one building is also appealing to those who live the country lifestyle.

Our rural lending experts have the answers to some of the most frequently asked questions when it comes to building your own barn home!

What are the benefits of building a barn home?

- Barn homes do not require interior load-bearing walls, resulting in their exceptional open floorplan designs and possibility for soaring high ceilings.

- Barn home exteriors or “shells” can often be built more quickly than a traditional home.

- Barn homes are sturdy and long-lasting; their steel exteriors can last up to 40 years hassle-free, unlike traditional homes that require regular maintenance

- Superior insulation options available for barn homes can result in higher energy-efficiency and reduced utility costs

- Depending on the design and materials used, barn homes can be more affordable than traditional stick-built homes.

Is a barn home always less expensive to build than a traditional stick-built home?

The cost of constructing a barn home depends on many factors. Like traditional homes, barn homes can range from small and simple rectangular designs, to huge, extravagant living quarters with complex rooflines, custom windows and spacious porches. The quality of materials used for flooring, walls, cabinets, windows, roofing, ceiling and lighting can all affect the final cost. In general, a barn home can be less expensive than a traditional home per square foot, but the cost depends on materials used, customization, amount of labor required and size of the home.

Does GreenStone finance barn home construction?

GreenStone offers financing options for the purchase or construction of barn homes of at least 1,000 square feet and that include at least two bedrooms. Financing options are available for up to 30 years for both the home and the home site.

How much is the down payment for a barn home?

At GreenStone, a standard down payment on a barn home is 20%. Some traditional home loans do qualify for PMI (Private Mortgage Insurance), which can be used to decrease the down payment to only 5%. If a customer is interested in a lesser down payment through PMI financing and they want to construct a barn home, they should consult with their financial services officer to ensure the scope of the property or project is in compliance with GreenStone and Enacts (PMI company) underwriting guidelines. The impact the appraisal may have on the cash needed for the complete down payment should also be considered.

A home’s expected appraisal value after construction, called “as will be” appraisal, is partially based on the value of comparable homes in the area. Because barn homes are still relatively new and less common, and few have been resold to date in most areas, it may be difficult for the appraiser to find comparable homes on which to base an accurate appraisal value. This may result in a conservative appraisal value below the actual cost to build the home. That difference will need to be paid in cash on top of the standard down payment.

How are barn homes taxed?

Barn home valuation may consider only the living areas of the building or could include the entire property, depending on the regulations in your city, township or county. It is a good idea to research barn home tax costs before construction begins to understand the long-term property tax requirements. You should always consult with your municipal tax assessor to best understand how taxes will be assessed for your future property.

What size and type of barn home can I build on my land?

Your county or township’s zoning regulations will inform what size and style your structure can be. If you intend to build a combined-usage barn home, a barn including both living quarters and a horse stable or living quarters and a public retail or service space, check with your local zoning authorities to confirm if combined usage is allowed. Variances on existing zoning are possible, but exceptions can be difficult and expensive to achieve.

What else should I think about when considering a barn home?

The native core structure of a barn home is different than a traditional home, resulting in some limitations to what one might normally expect with a home. Most barn homes are built on a cement slab foundation, not a basement, due to the post-frame construction style. Typically, if you desire to add drywall, extra framing is needed between the posts, which are usually placed eight feet apart rather than 18-24 inches for traditional homes; this can be an added expense. Insulation costs can be higher, as pole barn walls are thicker than typical stick-built homes (as a benefit, however, this can also result in lower heating and cooling costs). You may also need to add a vapor barrier to keep out moisture. Some builders consider this an upgrade.

Building a barn home can be an exciting and rewarding experience, resulting in a unique and enjoyable dwelling when the work is finished. Carefully researching and asking the right questions before construction begins can help ensure a positive outcome.

To learn more about building a barn home and GreenStone’s home construction loans, contact your local branch.