US Economic Outlook:

With the election over, what can we expect? The Republican party managed a trifecta win and will chart the economic course for the country. If campaign promises come to fruition, tariffs against China will surge, and there will be extensions of the Tax Cuts and Jobs Act of 2017, as well as tax cuts on Social Security benefits and overtime income. This could lead to a larger federal deficit, as the income from the new tariffs will lag the projected tax cuts. It will be imperative for additional action to be taken to achieve a stable fiscal policy and limit expansion of the deficit.

How will the Fed respond to the plans laid out by the new administration regarding future rate cuts and where the target fund rate should settle? Economic stimulation from proposed tax cuts will be buffered by the drag from the additional tariffs, allowing the Fed to continue additional rate cuts, while keeping a close eye on unemployment numbers and inflation. After the December rate cut, a couple of additional rate cuts are expected in each of 2025 and 2026.. The Fed is expecting the target fund rate to settle in the 3.25-3.5% range, a substantial reduction from the previous high of 5.2-5.5%.

Economists were nervous in July when the unemployment number jumped to 4.3%. However, in September the unemployment rate dipped back to 4.1%. The softening job market is a continuing trend as both private and government sector employment are growing at a slower pace. Unemployment is projected to continue to rise through the remainder of 2024 and stabilize at 4.4% second quarter of 2025 and the balance of the year.

Monetary and fiscal policy, along with global commodity price volatility due to supply disruptions and increasing civil unrest globally, will be the economic drivers heading into 2025.

Agricultural Economic Outlook – December WASDE and ERS Outlook Report

Corn:

The U.S. is coming off a successful growing season with a near record corn crop. The U.S. Grains Council Corn Harvest Report indicates that the quality of the corn crop is extremely high – excellent news for exports. December’s report estimates corn yield at 183.1 bushels per acre and total production at 15.1 billion bushels, unchanged from the previous report as harvest is essentially complete. There is good news as ethanol production has increased throughout the fall months. The Grain Crushing report shows the highest usage of corn for ethanol production from September to November since 2017. In addition, the Outlook for U.S. Agricultural trade released last month by the USDA raised projected corn exports by 200 million bushels. Higher domestic use and higher exports will lower ending stocks, however the forecasted season average corn price received by producers remains at $4.10 per bushel for 2024/2025.

Soybeans:

This month’s supply and usage report shows the 2024/2025 soybean crop figures unchanged from last month with total production of 4.5 billion bushels. Soybean oil production is projected to increase along with stronger export numbers which will drive ending stocks lower. However, global oilseed production was raised this month by 1.7 million tons to 427.1 million with increases in Argentina, Bolivia, and Canada. This will result in higher global ending stocks and continued negative pressure on US soybean prices. The USDA revised their season average soybean price received for the 2024/2025 crop sixty cents lower, now estimating $10.20 per bushel for soybeans.

Dairy:

Per the USDA milk production report, milk production was up 0.2% from October ’24 compared to October ’23. This increase was primarily driven by a larger U.S. dairy herd, expanding 46,000 head in the past three months, breaking a downward trend in the herd size that started in March ’23. Not coincidentally, the compressing herd trend, coupled with strong demand, has allowed for increased milk prices in the second half of ’24. The average Class III milk price for Q3 jumped to $21.26 compared to $17.97 in Q2 and $15.86 in Q1. The USDA dairy cull cows marketed through US slaughter plants are at the lowest point dating back to September 2007, suggesting dairy producers are keeping their cows longer days in milk or breeding for another lactation. This makes sense due to the smaller overall dairy herd (despite the recent increases) and higher demand for replacements due to the scarce heifer supply.

With production also up as yield increased by 3 lbs. to 1,996 pounds/cow, U.S. butter prices have declined 22% from their peak earlier this summer while CME spot cheddar barrels are down 48% from mid-September and blocks are 32% lower. Despite this pressure weighing on CME milk futures, it is making U.S. supplies more competitive in the export market. Class III milk futures for 2025 average $18.99 and Class IV milk futures average $20.65. These prices are slightly higher than the averages experienced in 2024, a profitable year for dairy production. Relatively strong basis continues as demand for new processing plants coming online persists. These milk prices, coupled with the drop in feed costs, should provide producers with an opportunity for solid margins into 2025.

HPAI continues to impact the industry as 248 cases have been confirmed in California in the last 30 days leading up to the end of November and 13 new cases in Utah. Since March 2024, 650 cases have been confirmed across fifteen states. Production in California has dropped as output dropped 3.8% year-over-year and total cows declined by 4,000 head in October. The USDA recently announced plans for mandatory animal testing for H5N1.

Pork:

Fourth quarter rallies in pork prices and improved producer margins are always welcomed but are also rare. The first 2 months of Q4 2024 have been unusually good due to a counter-seasonal upswing in the pork cutout, cash prices, and lean hog futures markets, coupled with lower corn and soybean meal prices. Entering December, the outlook for margins over feed for producers for the next four quarters is stronger than for most periods over the past decade. Producers are increasing hedging activities and purchases of LRP policies to lock in some of these surprising margin opportunities. The Pork Cutout is up 7% vs. a year ago, led by increased ham and belly prices. Retail prices for pork are at the highest levels since Q4 2023 at $4.92/pound at the end of October.

Export demand remains solid with volumes up 5% vs. a year ago through September and export values up 7%, with exports to Mexico leading the way. The September USDA Quarterly Hogs and Pigs Report showed an increase of 4.3% in heavy weight hogs. However, hog numbers marketed since that report have not matched up. Pork inventories are at a 20-year low for the end of October and down significantly from a year ago. The previously strong demand for bellies is waning, which will negatively impact Cutout price.

Disease pressure may further limit supplies as fewer than expected head have been marketed in recent weeks and carcass weights have not increased as much as they often do seasonally. Live hog weights have been below 2023 weights and the 5-year average over the past several weeks. While a stronger finish in 2024 will make for a much better year for producers and provide cautious optimism for 2025, it has still been a challenging year and average returns per hog sold will vary widely based upon herd health, production efficiency, packer contract type, and the timing and degree of price risk protection utilized.

To view the winter 2025 issue of Partners magazine in its entirety, click here.

It’s Patronage time for GreenStone’s cooperative members, and the members elected to the Board of Directors are pleased to approve another $120 million back. For 20 years GreenStone has returned profits back to members through the Patronage program, and this year’s return will bring the total to more than $1 billion back in member’s hands. This billion means more than the dollars returned, and your board members took the opportunity to share their perspective of what that $1.08 billion means to them!

Gene College,

Appointed Director

A billion dollars – if every employee conversation about how to serve our customers more effectively was worth $1,000, that makes one million thoughtful dialogues!

Michael Feight,

Lenawee County, MI

A billion dollars of Patronage. A true sign of how a cooperative was designed to work. The staff at GreenStone is doing their part to help you realize your goals that move from generation to generation.

Terri Hawbaker,

Clinton County, MI

GreenStone’s ability to distribute a record setting billion plus dollars in Patronage simply validates their efficiency, and the program’s procedure by keeping the cooperative healthy first then maintaining competitive rates to its members. The Patronage program ensures GreenStone will be there for many generations to come!

Trent Hilding,

Montcalm County, MI

GreenStone creates a lot of opportunities in providing the money it loans and returns to its customers. It is hard to grasp a billion dollars has been returned to borrower members, but I am grateful for the opportunity to participate.

Bruce Lewis,

Hillsdale County, MI

A billion dollars of Patronage returned to our members in twenty years. What a wonderful event. What a great organization we have that not only is there daily to help with our needs but also there to give back year after year.

Ron Lucas,

Alpena County, MI

As you meet your fellow shareholders on Patronage Day, they are all appreciative to get a Patronage check back. Most can’t believe we’ve given back that much!

Peter Maxwell,

Midland County, MI

I reflect on one billion dollars and think of a popular fast-food chain that used to say millions served, then posted over one billion served and eventually used the line, billions and billions served. I look forward to our future when we can say billions and billions returned. I certainly know the returns we send directly back to our shareholders are impactful and am personally grateful!

Dave McConnachie,

Sanilac County, MI

Owners of the cooperative know what a billion dollars in Patronage returns means to their farms. As a director, I know it’s a direct response of the health of GreenStone. And I’m confident the next twenty years will be even better.

Dennis Muchmore,

Appointed Director

Over the twenty years I’ve been fortunate enough to be included on the GreenStone Board, I‘ve seen first-hand what a billion dollars of Patronage can mean to our members and our agricultural community at large. This exceptional co-op has created a billion dollars of reinvestment, a billion dollars of leadership and with apologies to the original lyricist for a slight alteration in an old song, “Greenstone has walked a billion miles for your smiles.”

Ed Reed,

Cass County, MI

The last 20 years have been successful in a billion ways. I can think of a billion reasons to be part of the GreenStone family. What has a billion dollars meant to the 28,000 GreenStone cooperative members? About 100 basis points – 1% – returned to them as cash Patronage.

Go GreenStone!

Scott Roggenbuck,

Huron County, MI

A billion is a large number. A billion seconds is 32 years.

It took around 20 years to reach the milestone of a billion dollars of Patronage paid out to our members. However, at the current pace we could reach the second billion before half that time expires. Patronage, just one more thing that sets GreenStone apart from the competition.

Troy Sellen,

Oconto County, WI

For 20 years GreenStone has given us cash to put back into our homes, communities and businesses. Patronage is more than a bonus check. It’s a billion different examples that prove the cooperative structure of Farm Credit lending works.

Marilyn Thelen,

Clinton County, MI

The billion dollars returned to customers over 20 years is an indication that GreenStone is doing well and when they do well, they share this back with the members. This is a “thank you” to the members. It takes good members working with GreenStone to be successful. Farmers big and small will be very appreciative of the check this March.

Mike Timmer,

Allegan County, MI

While GreenStone appreciates the relationships it has with our shareholders, nothing says, “thank you, we have been successful together,” like Patronage. One billion over 20 years… Wow!

Dale Wagner,

Manitowoc County, WI

Returning a billion dollars of Patronage to our members is an impressive milestone. However, to me what’s even more important is the effort put in by every employee and member borrower to do their job well, to operate their business efficiently and to work together as a team so we all can be successful. This is why, as a GreenStone director, I would like to offer a billion Thank Yous.

Jed Welder,

Montcalm County, MI

I always appreciate the timing of Patronage. It’s well after the harvest but before our large expenditures during planting season. It’s also a time to reflect on our profession before we get too busy to consider anything other than the placement of the seeds going into the ground!

To view the winter 2025 issue of Partners magazine in its entirety, click here.

For Tanner and Mariah Sharp, 2024 was a life-changing year. In November, the couple officially adopted their two daughters, Ella and LeeAnn, completing their dream of becoming a family of four.

With this milestone celebrated, they were eager to move out of town and begin a new chapter in the countryside. They envisioned their daughters growing up on a property with plenty of room to run around and play outside.

On the outskirts of the small town of Rosebush, Michigan, the Sharps fell in love with a five-acre hobby farm, complete with a mid-1920s stone farmhouse, a pole barn and of course, plenty of space for the girls to explore and play.

The property was perfect, but just as they approached the finish line in the home-buying process, their previous lender unexpectedly backed out of the deal. The reason? A windmill lease tied to the property. The news came just days before closing, leaving the Sharps discouraged and scrambling to find a solution.

“We found out two or three days before closing that our lender wasn’t going to finish the loan,” Tanner Sharp said. “It was pretty disheartening.”

Turning to GreenStone for Help

With limited options and a fast-approaching deadline, the Sharps turned to GreenStone. Both Tanner Sharp’s parents and his brother and sister-in-law were GreenStone customers and had positive experiences working with the team. Encouraged by their recommendations, he reached out to Financial Services Officer, Jordan Hendrian.

“I got Jordan’s contact information from my sister-in-law, and I explained the situation to him,” Tanner Sharp recalled. “Jordan said, ‘Let’s talk over the details and see how fast we can turn this around.’ From that point, everything moved quickly.”

A Race Against Time

GreenStone’s team immediately got to work to make sure the Sharps got into their dream home. Typically, closing a home loan takes about 30-35 days, but the Sharps didn’t have that kind of time. They were set to sell their current home in a few days, and without a solution, they faced the very real possibility of being left without a place to live.

“Everyone—from the appraisal team to the loan processors—worked on all cylinders to make this happen,” Hendrian explained. “We knew this was a priority, not just to get the deal done, but to ensure the Sharps had a place to call home for their family.”

In just 17 days, GreenStone closed on the loan. To make it happen, the team coordinated with the title company to transfer the necessary documents into GreenStone’s name and successfully transferred an existing appraisal to save the Sharps time and money.

“Jordan was on the ball,” Tanner recalled. “He told us exactly what he needed, and we got it to him right away. GreenStone’s communication was by far superior to anything we’d experienced before. They kept us informed every step of the way.”

The team even worked with the seller’s realtor to allow the Sharps to rent the property while the loan was being finalized, ensuring they could move in right after selling their previous home.

Starting a New Chapter

Now settled into their forever home, the Sharps are loving life in the countryside. They’re enjoying the charm of their historic stone farmhouse and have plans to update the home while preserving its vintage woodwork and character. More importantly, they’re cherishing this time as a family, creating memories with Ella and LeeAnn in a space they can call their own.

“GreenStone turned a stressful situation into a seamless experience,” Tanner remarked. “They were the reason we were able to close so quickly and start this new life on the farm. We couldn’t have asked for a better partner.”

For the Sharps, the experience reinforced the importance of working with a lender they could trust.

“Jordan went the extra mile to make sure everything went smoothly,” Tanner added. “He even ensured the appraisal didn’t cost us anything extra. GreenStone proved they were willing to do what it takes to make things work.”

A Team Effort at GreenStone

For Jordan, the Sharps’ story is a testament to what’s possible when everyone works together.

“To pull off a 17-day closing takes dedication on both sides,” he said. “Tanner and Mariah were incredibly responsive, getting everything back to us within minutes. Their realtor was fantastic, and everyone at GreenStone worked tirelessly to make this happen.”

Jordan also noted how the collaboration highlighted GreenStone’s unique ability to navigate unexpected challenges. “It was rewarding to hear the Sharp’s realtor say, ‘I know we can go through GreenStone without any issues.’ That trust in us made a big difference.”

GreenStone’s Commitment to Making Dreams Happen

For GreenStone, the Sharps’ story is more than just a story about a successful loan—it’s a reflection of their mission to support rural families and their dreams.

“This was a win for everyone involved,” Jordan said. “It showed what we can accomplish when we put our heads together and focus on helping families like the Sharps achieve their goals. It’s moments like this that remind us why we do what we do.”

Thanks to GreenStone, the Sharps can look forward to many happy years in the country—creating memories, raising their daughters and living out their country dreams.

To view the winter 2025 issue of Partners magazine in its entirety, click here.

As the ice starts to form on the local lakes and frosty mornings become the norm, I try to take some time during the winter months to reflect on the previous year. Part of that process involves looking back on the past hunting season. Every year I make an effort to take note of the highs and lows along with what I did well and what I could have done better. As I reflect on the 2024 hunting season, I can’t help but smile as I remember the year that was.

As a hunter myself and a producer for Michigan Out of Doors TV, life during deer season is pretty chaotic. Regardless of how present I try to be for every day in the field, the days just seem to slip away faster as the years go by. That was especially the case over the past year. In addition to the normal fast paced life of working and parenting, my wife and I were also expecting our third child in December. If that wasn’t enough, we broke ground on our new house a couple of months before the season started. As the hunting season approached, I remember worrying about how much time I would get in the field throughout the fall with everything we had going on in this season of life. As I look back, it’s easy to see why I was concerned.

The archery season actually started out pretty slow. My time was somewhat limited over the first few weeks of October, but the weather was warm and windy, which had the deer movement at a minimum. So, I wasn’t too concerned about missing time. As the season progressed, I started getting pretty consistent trail camera pictures of the oldest known buck on our farm. A 5 1/2 year-old eight point that I knew well from the previous two seasons. I hunted him hard throughout October and had multiple encounters with him. I actually had him within range on three different occasions but never could get an ethical shot.

As November rolled in, he disappeared for about a week only to return again on November 6th. Early that morning, one well placed arrow helped me put a tag on my oldest buck to date. At that point, the season was already a success. Taking any mature buck with a bow and arrow is an accomplishment and I was already completely content with my season. Although this buck didn’t score quite as high as some of the other deer I have taken, the back-and-forth during bow season along with the history I had with this buck made for one of the most enjoyable hunting seasons I have ever had. However, around the time I was able to close the chapter on that buck, a bigger buck moved in. A buck that I knew would be my biggest to date. I took a couple days off to get caught up on things around home. However, that was short-lived. With my wife’s blessing, I refocused on the new buck and the chase started all over again.

Over the final week of bow season I hunted every day, having multiple encounters with the new buck. Unlike the first buck, I couldn’t seem to figure out how to get within bow range of this deer, or even close to it. Throughout that week, I hunted six different locations, including three new tree stands that I hung specifically for him. He was living in a heavily used bedding area and getting within range of him was difficult. With the high deer densities of southern Michigan, he was constantly surrounded by a harem of does.

On the night of the 13th, the last night I was able to bow hunt, I decided to take a calculated risk and hunt a new spot in his home area. Long story short, I ended up sitting on a platform of an old gun blind about 8 feet off of the ground. It wasn’t pretty, but it was effective. Around 4:30 in the afternoon the buck presented me with a 30 yard shot and I was able to make the most of it. He was indeed my biggest to date and capped off an incredible year in the timber.

Just when I thought my season couldn’t get any better, it did. On the opening day of gun season, November 15th here in Michigan, I was able to take my 88-year-old grandpa out for the morning hunt. He tagged a beautiful eight point to put a bow on what really was a year for the books. As an extra bonus, I was able to capture the entire hunt on camera which made for not only a memorable segment on the show, but a memory I can relive over and over again.

When my wife and I purchased this piece of property a few years back, it was hard not to think about what was to come. A constant battle of being present and also planning for the future. Here we are two years later expanding our family, building a new home, and creating memories we will never forget. This year was not only a dream season from a hunting standpoint, but from a life standpoint. I can’t imagine a time where we will ever be busier than we are now, but it only takes a little time to reflect on what we have to realize that we’re already living the life we always dreamed of.

To view the winter 2025 issue of Partners magazine in its entirety, click here.

Family Resolutions

The holidays are a wonderful relaxing time for the whole family to spend time together, celebrate the past year, and look forward to the future. Often when looking forward to the new year, we set individual New Year resolutions. However, these goals tend to be hard to follow for the entire year. After about a month many often lose track of these resolutions and cannot keep them up to the same standard we intended to.

An issue with these resolutions is that they are independent. Keeping track of a busy schedule and new goals by yourself can be hard to navigate. Accountability partners have been shown to provide extra motivation and support to accomplish your goals.

Taking all of this into account, what if we did family resolutions? These could focus on quality time, kindness, acts of service, or anything specific your family sees as a need for the new year. Taking the time to sit down together and hear everyone’s thoughts on what should be included and how you can accomplish these goals together.

1. What goals or resolutions should you set? A baseline could be one for each member of the family!

2. How will you keep each other accountable? Will you do weekly check ins?

3. What is the timeline for each of the goals? Where do you want to be at this time next year?

Guiding conversation like this could help shape your expectations for these new goals. Taking time together to outline all milestones and expectations up front will provide a clear path to accomplishing each goal you set. Each milestone should serve as a step of progress for all resolutions. At each milestone you can find a different way to celebrate all progress. Something that would interest everyone and encourage the family to finish the goal – perhaps a homemade trophy, candy, or a game night!

It’ll also be important to plan what the whole family wants to do in celebration of seeing the resolutions all the way through. Something special to congratulate yourselves on all of the hard work it takes to stay consistent as a unit throughout the year! Consider a picnic at the park, dinner at your favorite restaurant, or homemade sundaes to celebrate your success. Collaborating as a family can help everyone to feel included, on track, and connected to accomplish these goals together.

We hope your family is able to set and accomplish these resolutions for 2025, teamwork makes your dreams work!

To view the winter 2025 issue of Partners magazine in its entirety, click here.

As winter continues to gear up, snowmobiling across the icy trails of Michigan and Wisconsin is increasingly popular.

Winter is filled with snow, chilly temperatures, and fun memories outside. Snowmobile riding is a big piece of the winter fun for many, and here are a few tips to make sure all the fun stays safe!

Riding Tips

Whether you’re on the trail, road, or hilly terrain, it’s important to understand how to maintain control of your snowmobile throughout your trip. Understanding your path of travel is crucial as it can be hard to steer or stop a sled that is sliding. Keeping a clear path and planning your route will help you ensure safety and keep you heading in the right direction! Shifting your weight from one side to another can help you maintain balance, especially during turns. Slowing down and shifting your weight to the inside of the turn will help you accelerate after and maintain control.

Wearing the Right Gear

All it takes is one wet layer to put a damper on the adventure. Making sure you have the proper underlayers, like thick socks and long sleeves can go a long way. Merino wool is known to be a good material for underlayers because the wool is capable of wicking away moisture from the body, unlike cotton which causes moisture to stick around. Waterproof gear is key, having the proper coat and boots to keep yourself insulated and dry on top of these underlayers is important. No matter what gear you have or don’t have, the most important piece of a snowmobile is the helmet. Ensuring you have a full-face snowmobile helmet will be the key to safety. A snowmobile helmet has a dual pane system to protect faces from frostbite and prevent fog. This will keep you safe and comfortable for your ride!

Adapt to Changing Conditions

Depending on the weather, the snow can easily change from hard-packed to deep powder throughout the day. Prepare by monitoring the snow conditions to adjust your route to fit. Driving in deep powder can be challenging when going uphill consistently, preparing for that challenge or adjusting to a more flat route during these conditions may be ideal. Hard-packed snow allows you to easily gain speed and momentum, but it is also much harder to come to a stop. Maintaining control on hard-packed snow may be considerably more difficult, so adjusting your route to take less turns may be beneficial.

Using tips like these can help keep your winter memories fun and exciting each time you head out to enjoy the season!

To view the winter 2025 issue of Partners magazine in its entirety, click here.

Indulge in this classic treat with a Sharp family twist for the most delicious, ooey-gooey chocolate chip cookies you’ve ever had! Pair with a chilled glass of milk for the perfect cold winter night’s snack.

Total Time: 25 minutes

Serves: 9-12

Ingredients

- 8 Tbsp salted butter

- ½ cup white sugar

- ¼ cup light brown sugar

- 1 tsp vanilla

- 1 egg

- 1 ½ cups flour

- ½ tsp baking soda

- ¼ tsp salt

- ¾ cup chocolate chips

Directions

1. Pre-Heat oven to 350°

2. Melt butter

3. Beat butter with both sugars

4. Add vanilla and egg; beat on low for 10-15 seconds (not too long, beating the egg too long will make a stiff cookie)

5. Add flour, baking soda, salt and chocolate chips

6. Mix until crumbles form

7. Use hands to form dough into ball

8. Roll into 9- 12 small balls

9. Bake for 9-11 mins (any longer will make them tough) Enjoy your Sharp family cookies!

To view the winter 2025 issue of Partners magazine in its entirety, click here.

For Boyd and the Endsley family, ECO is more than just an insurance option—it’s a way to ensure the resilience and success of their farm for generations to come.

Navigating Risk in Modern Farming

As any farmer knows, managing risk is an essential part of running a successful operation. For Boyd Endsley, a livestock farmer in Barry County, Michigan, balancing risk and reward has been a constant focus in his family’s multigenerational farming business. When it came to mitigating price volatility in 2023, Boyd turned to GreenStone and an Enhanced Coverage Option (ECO) as a part of his crop insurance policy to help secure his farm’s financial stability.

“In 2023, we decided to add ECO coverage because we saw a lot of potential for crop prices to drop, which could trigger an ECO payment,” Boyd shared. “We wanted to manage that risk, and it ended up being a good decision for us.”

How ECO Provides Protection

ECO, an additional layer of crop insurance, provides coverage from 86% up to 95% of a county’s expected yield or revenue. Unlike traditional crop insurance policies, ECO is designed to protect against county-wide yield and revenue losses. With the subsidies for ECO increasing from 44% to 65% in 2025, this highly affordable option gained popularity among farmers who were looking to navigate an unpredictable agricultural market.

For the Endsleys’, 2023 demonstrated the value of ECO firsthand. While Barry County’s average yield for corn exceeded expectations at 166.1 bushels per acre—above the projected yield of 161.8—a significant drop in the harvest price, from $5.91 to $4.68 per bushel, triggered an ECO payment. This additional income proved invaluable in a year when commodity prices were down.

“In a year when our income was lower because of declining prices, the ECO payment provided critical support,” Boyd explained.

Trusted Guidance and Strategic Decisions

Boyd’s decision to adopt ECO came with the guidance of Kristen King, his crop insurance specialist at GreenStone. Kristen has worked closely with the Endsley family for more than a decade, helping them navigate the complexities of crop insurance and other financial tools to support their operation and mitigate risk.

“Kristen is incredibly knowledgeable and always on top of her game,” Boyd said. “She knows the products inside and out and can explain how they work in different scenarios. She’s great at making sure I have everything turned in on time and keeps me informed about all my options.”

For Kristen, Boyd’s approach to ECO exemplifies strategic risk management. “Boyd is an intelligent guy who really pays attention to the numbers,” she said. “He’s not someone who’s going to take ECO every year—he evaluates the market and decides based on the potential for price declines. That’s where ECO really shines. It’s highly subsidized and provides great coverage in years when there’s significant price risk.”

Balancing Coverage Across Crops

In 2024, Boyd opted to continue using ECO for his soybean crop, anticipating further price declines in that market, while choosing not to apply it to his corn, which he believed had less downside risk.

“Soybean prices looked like they might continue to decline, so we decided to keep ECO on that crop,” he said. “Corn, on the other hand, didn’t have as much room to drop, so it didn’t make as much sense to use ECO there this year.”

A Legacy of Resilience

The Endsley family’s farm is a true legacy operation, with Boyd working alongside his parents, Patricia and Gordon, to grow corn, soybeans and wheat, as well as manage a cattle herd that has been part of the farm since 1955. Boyd’s commitment to thoughtful risk management and strong partnerships has helped him carry on that legacy while adapting to the challenges of the modern agricultural climate.

The Future of ECO and Risk Management

Looking ahead, both Boyd and Kristen see ECO as a valuable tool for farmers who want to protect their operations against market uncertainty. “With the increased subsidies in 2025, ECO was even more affordable and attractive to farmers who anticipated price volatility,” Kristen said. “It’s a flexible option that can really make a difference in the right conditions.”

Boyd agrees. “For us, ECO provided stability in a year when we needed it,” he said. “We took ECO again in 2025, and will continue to see if it is an affordable long-term option to insure against the top 10% of our risk”

As GreenStone continues to offer ECO as part of its comprehensive risk management offerings, Boyd’s story highlights how strategic decisions and trusted partnerships can help farmers weather the ups and downs of the agricultural industry. For Boyd and the Endsley family, ECO is more than just an insurance option—it’s a way to ensure the resilience and success of their farm for generations to come.

To view the winter 2025 issue of Partners magazine in its entirety, click here.

Wisconsin businesses –

You can take comfort knowing this change is for Michigan businesses only.

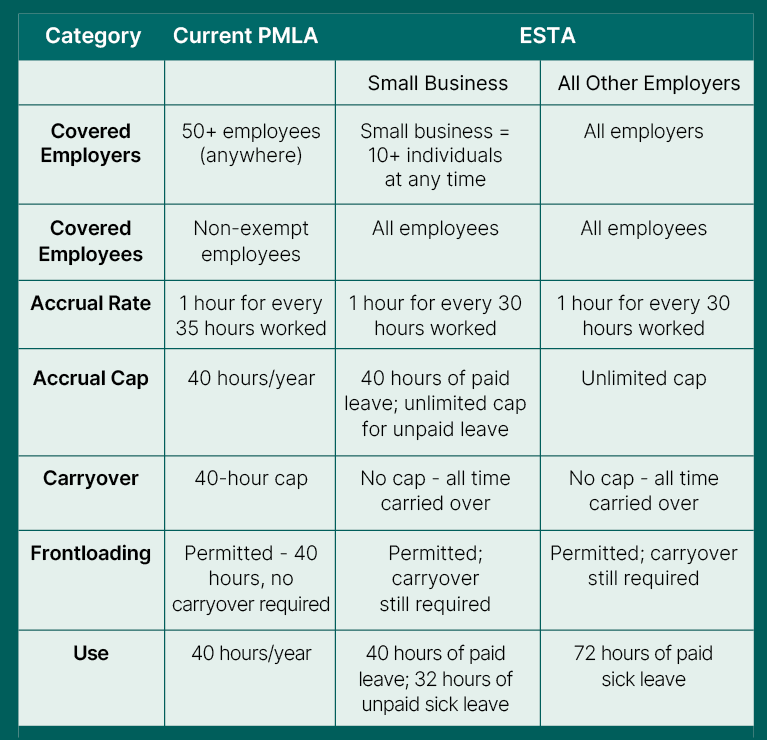

Starting on February 21, 2025, every Michigan employer, regardless of size, must provide their employees with up to 72 hours of sick leave annually under Michigan’s new Earned Sick Time Act (ESTA) – this includes agriculture employers and employees! On November 12, 2024, several agricultural organizations, including GreenStone Farm Credit Services, wrote to the Michigan legislature with their concerns related to the ESTA’s impact to the state’s agriculture industry. The letter can be found here. Michigan employers have been administering a paid leave law for the last five years under the Michigan Paid Medical Leave Act (PMLA) – many were not impacted by this law because it only applied to employers with 50+ employees. However, on July 31, 2024 the Michigan Supreme Court reinstated a voter initiative known as the ESTA which drastically changes the landscape for Michigan employers to provide sick time to employees. The ESTA is the original version of a law adopted by the Michigan legislature that was immediately amended to create the PMLA, a more limited sick leave program applicable to many Michigan employers since 2019. By court order, the ESTA will take effect on February 21, 2025, replacing the PMLA and covering all Michigan employers.

This article provides a summary of the changes under ESTA, highlights answers to some frequently asked questions (FAQs) and outlines some items you should do now to ensure compliance when ESTA takes effect on February 21, 2025. Most of this information presented is taken from the State of Michigan’s Labor and Economic Opportunity (LEO) website on the ESTA. The website has many resources you should familiarize yourself with – including a link to the act, FAQs, posting requirements, brochures, etc. The website can be found here.

Who Is Covered Under the ESTA?

All Michigan employers, except the U.S. government, must adjust or implement policies to comply with ESTA requirements. ESTA applies, regardless of industry, to employers that employ one or more employees in Michigan – employers are split into “Small Business” and “All Other Employers” as defined by the LEO.

All employees are eligible, regardless of classification to receive earned sick time.

What is the accrual rate for earned sick time?

Beginning February 21, 2025, or upon the employee’s start date, whichever is later, employees will accrue 1 hour of sick time for every 30 hours worked. Employers may require new employees to wait 90 days after hire to use accrued sick time, but the accrual begins immediately upon hire.

How much earned sick time are employees entitled to?

Small businesses must provide up to 40 hours of paid earned sick time, with an additional 32 hours unpaid. All other employees must provide up to 72 hours of paid earned sick time per year. You should review the LEO website to determine if you are a small business or not.

Does earned sick time carry over?

Yes. All accrued and unused sick time must carry over to the following year. ESTA does not impose a cap on accrual or carryover.

Can employers frontload the earned sick time?

Yes. Employers may frontload the full year’s worth of sick time at the beginning of the benefit year. However, the frontloading method implemented must comply with the ESTA’s accrual, usage, carryover, and other provisions.

Does unused earned sick time have to be paid out at the end of a calendar year or employee termination?

No. ESTA does not require employers to payout unused time. Employers should check and confirm their written policies align with their desired practices concerning payout, as separate written agreements or policies may require employers to pay these amounts out.

As Agricultural Employers – What Should We Do Now?

Although the ESTA is not scheduled to go into effect until February 21, 2025, Michigan agriculture employers can mitigate their risk by taking steps now to make sure they are in compliance with the ESTA come the effective date. At a minimum, the following actions are recommended:

- Become familiar with the ESTA information on Michigan’s LEO website. Additionally, watch for new ESTA guidance and regulations on Michigan’s LEO website.

- Review and revise vacation, sick and other leave-related policies, including onboarding notices, timekeeping, and payroll mechanisms, to comply with the ESTA’s requirements.

- Ensure human resources personnel understand the rights and protections afforded to employees under the ESTA, including administration of all vacation, sick and other leave-related policies, notice and posting requirements, and recordkeeping obligations.

- Train all supervisor employees to avoid retaliating against an employee because the employee has exercised a right protected under the ESTA.

- Obtain and timely display copies of the required ESTA posters.

To view the winter 2025 issue of Partners magazine in its entirety, click here.

As we kick off the new year, it’s important to refresh ourselves on the cybersecurity topics we’ve explored over the last year – topics we hope provide you with practical, actionable advice to keep your family, finances, and operations safe. Cybersecurity can often feel intimidating or overly technical, which is why we provide these tech tips and work to break these subjects down into simple, human terms.

Whether we are discussing emerging threats such as AI-driven deepfakes, providing guidance on identifying financial scams, or shared recommendations on password management and multifactor authentication, the objective has remained the same: to make cybersecurity comprehensible and actionable for everyone.

AI and Deepfakes: The Threat Feels Like Science Fiction

Over the last 12 months, AI and deepfakes dominated the headlines and for good reason. Just a year ago, most of us were not even talking about deepfakes. Today? They are everywhere, just take OpenAI and their new tool Sora that can create hyper-realistic videos and audio clips that are so convincing they can fool even the sharpest eye. Imagine receiving a video call from someone who looks exactly like your trusted financial advisor, but it’s not really them.

In the Fall Partners Magazine titled The New Era of Financial Fraud – Deepfakes and AI, we shared, “Threat actors are using deepfakes and AI-generated content to manipulate communications, impersonate trusted individuals, and trick people into harmful financial decisions.”

It’s a terrifying reality, but there’s good news: you can take steps to protect yourself. Start by enabling multifactor authentication (MFA) on all your accounts. MFA adds an extra layer of protection, making it much harder for attackers to gain access, even if they trick you into revealing a password.

Mail Scams and Public Information: Too Real to Ignore

Have you ever received an official-looking letter in the mail about your mortgage, farm equipment, or property taxes that seemed a little… off? You are not alone. In Summer Partners Magazine, we covered this growing problem in Scammers and Public Information – Be Informed.

The short version? Cybercriminals are digging through public records—like court filings and property deeds—to send out fraudulent mail that looks incredibly legitimate. It might say you owe money, need to act quickly, or it could even offer tempting deals on equipment or loans.

Here’s what was suggested back then, and yet today: “Public records can be exploited to create mailers that mimic official correspondence, tricking recipients into taking action.”

So, what can you do?

- Trust but verify: Don’t act on any unsolicited mail until you confirm the sender’s identity.

- Shred sensitive documents before tossing them out.

- Use a locked mailbox to protect incoming mail.

And remember—if it feels rushed, urgent, or just too good to be true, pause. Scammers often use fear or excitement to push you into making hasty decisions.

Your Smartphone: A Double-Edged Sword

Let’s be honest—our smartphones are indispensable. They help manage farm operations, check finances, keep us connected—and yet, they are a goldmine for cybercriminals. If a bad actor gains access to your phone, they can grab everything: emails, passwords, bank info, you name it.

In the Spring Partners Magazine article, Five Tips to Secure Your Smartphone Now, these risks were explained: “Portability, constant connectivity, and access to sensitive information make smartphones a prime target for attackers.”

But do not worry, securing your phone is easier than you think. Start with these basics:

- Use strong authentication, like fingerprints or facial recognition.

- Regularly update your phone and apps—updates patch security holes.

- Be cautious about what you download. If an app looks sketchy, it probably is.

A few small tweaks can go a long way toward keeping your personal and financial information safe.

Looking Ahead throughout 2025

Cybersecurity is not about perfection—it’s about progress. The key is to take small steps, focus on what matters most, and build from there. Here are some recommendations worth starting in the new year:

- Passwords: Create unique, strong passwords for a few key accounts—like email and online banking. Once you get comfortable, a password manager can help you generate and store stronger passwords across more sites.

- Multifactor Authentication (MFA): Start with your most critical accounts and enable MFA. You’ll be surprised how much protection this simple step adds.

Thank you for continuing to join us on this cybersecurity journey. Our hope is that these tips have made you feel more confident and capable when it comes to protecting yourself. Here’s to staying vigilant—and ready—for whatever 2025 has in store.

To view the winter 2025 issue of Partners magazine in its entirety, click here.