A fifth-generation farm is a testament to an enduring legacy and resilience, a rare gem in today’s rapidly changing world. With each passing generation, the challenges and complexities of maintaining a family farm also evolve, making the survival and prosperity of such farms an extraordinary achievement. These farms are more than just businesses; they are living histories, where the knowledge and values of those who came before are cultivated alongside the crops.

Reaching the fifth generation is not just a milestone, it’s a celebration of tradition, commitment and the unbreakable bond between a family and its land.

Huehl Acres is a fifth-generation farming operation in Freedom Township, Michigan, which is located between Chelsea and Manchester. It is owned and operated by brothers Gerald and Dennis Huehl and their wives Carol and Susan.

The original farm has been in the family since 1839, when the brothers’ great-great-grandfather, John Huehl, started with 20 acres. The farm has now expanded to 417.5 acres owned and a total of 1,500 acres that are farmed for corn, soybeans, wheat and hay.

The Next Chapter for Huehl Acres

“Mom sold the cows after our dad passed away, and in 1976, we decided we wanted to get back in the dairy business,” Gerald said. “We milked cows for 41 years.” They produced and sold milk until April 2018 when the last of the cows left.

Previously a dairy farm, Huehl Acres now focuses on cash crops and specialty farming work, such as hauling grain or custom combining for other farms.

Along the way, the brothers have continued to grow the operation into what it has become today.

“We borrowed money from Federal Land Bank, which later became GreenStone, in 1979 to buy the next farm,” Dennis said. “We used to joke that we went in to borrow $100-200, and then rounded it up to the nearest $10,000 and then rounded it up to the next $100,000.”

Working the Figures

The Huehls’ relationship with GreenStone’s tax and accounting team began in 1981—only a few years after the cooperative launched its tax services division.

“Our computer goes back to 1989,” Gerald said. “Before that, we filled out the paperwork and sent it in every month to GreenStone. We always like the fact that we go in and spend a couple hours one morning at GreenStone every year, and other than a form or a phone call, that’s all the time we’ve had to put in to get our taxes done,” Gerald said. “It’s simple and stress-free. We’ve been very happy with it.”

Planning Pays Off

The Huehls prefer to do tax planning before the end of the year. The brothers also shared that the tax accounting service GreenStone provides is convenient because they are able to share the information with their financial services officer, eliminating one set of paperwork they need to supply.

The brothers said that GreenStone has been especially helpful the last few years as they transitioned to cash crop farming as they were able to do preplanning to minimize the tax burden as much as possible.

The brothers’ sons, Robert, Thomas and Nicholas Huehl, have all shown interest in the farm, which means the next exciting hurdle will be to work the farm into the sixth generation of the Huehl family.

“Farming is more than a livelihood; it’s a legacy,” Gerald said. “One day we’ll pass on the seeds of tradition and let the future harvest be even richer.”

As the Huehls look to the future of the farm, GreenStone is happy to continue to work with them and help ensure the success of their operation.

To view the fall 2024 issue of Partners magazine in its entirety, click here.

As we approach the fall harvest season, we thought it might be a good time to suggest one possible way for farming business owners to save on taxes while also investing in your family’s future – by paying your kids! As a family farm, many of you employ your children on the farm. Not only does it instill excellent work ethic and provide business knowledge, but if you employ your children you can save on taxes and help your children create wealth for later in their lives by using a custodial Roth Individual Retirement Account (IRA) on their behalf.

How could a Custodial Roth IRA Ensure My Next Generation is a Millionaire?

The S&P 500 has averaged an annualized growth of 10.13% since its inception in 1957 through 2023.

Scenario: If your child earns at least $7,000 annually in wages for work performed on your farming operation between the ages of 12 and 22, and all of those amounts are contributed to a Roth IRA account ($77,000 in total Roth IRA contributions over an 11 year period) – your child could have over $1,000,000 stocked away in a tax-free account for when the child turns 60.

In the above scenario, a Roth IRA account balance for your child at the age of 60 would be greater than $1,000,000 if the account experiences 6.50% in annualized growth. If the account grows 9.50% annually, the account would have close to $4,000,000. Approximate balances at different levels of growth rates over the almost 50 year time period are presented in this example:

Growth Account Balance

6.50% $1,177,880

7.50% 1,771,545

8.50% 2,656,591

9.5% 3,972,240

How does an account grow to this large of a balance off of just $77,000 in contributions? Compound interest! The earlier you start, the longer you have until your retirement age to reap the benefits of your account growing exponentially due to interest more or less building upon itself over time.

So… what is a Roth IRA?

A Roth IRA is a retirement investment account that anyone with earned income can contribute after-tax earnings. Investments in a Roth IRA account grow tax free. A custodial Roth IRA is when a parent or other adult opens one for a minor. At age 18, the child becomes the owner of the account. It should be noted that Roth IRAs can have fees associated with them, so be sure you understand those before opening an account.

A Roth IRA is different than a traditional IRA. With traditional IRAs, you deduct contributions now and pay taxes on withdrawals later, while Roth IRAs allow you to pay taxes on contributions now and get tax-free withdrawals later.

What are the requirements of a Roth IRA?

A single filer with an adjusted gross income under $146,000 per year, regardless of age, is eligible to contribute to a Roth IRA account. Roth IRAs allow anyone with earned income, such as farming wages, to contribute after-tax dollars. People can contribute up to the annual limit ($7,000 for individuals under the age of 50 in 2024) or the total of their earned income, whichever is less. Contributions to a Roth IRA are not tax deductible. There is no need to worry about making annual contributions as there is no mandatory funding requirement for Roth IRAs. Note that income and contribution limits adjust annually and vary based on age, and marital status. You can look online at the IRS rules each year to see how the wage and contribution limits change as most years these numbers are adjusted due to inflation.

How is payroll to a child treated?

Your farming business gets a tax deduction for child wage expenses. The deduction reduces your federal income tax bill, your self-employment tax bill, and your state income tax bill, if applicable.

Additionally, your child’s wages when they are under the age of 18 may be exempt from social security taxes, medicare tax, and federal unemployment tax depending on the structure of your business. Your child can ultimately shield up to $14,600 of wages from any federal income taxes during 2024. It should be noted that there will be state income taxes due – but those are taxed at a much lower percentage.

One caveat to cover regarding hiring your child – your child’s wages must be reasonable for the work performed. You need to maintain the same records as you would for any other employee to substantiate the hours worked and duties performed. This includes timesheets, job descriptions and W-9 forms.

Savings vs. 529 vs. Roth IRA

There are other options for you to consider if you are employing your child and have monies you want to save on their behalf – should they simply put their wages into a savings account, a 529 education plan, or the Roth IRA account we have discussed so far?

A traditional place for families to put a child’s earnings is in a savings account. Savings accounts are likely to have a lower rate of return when compared to a 529 or Roth IRA.

A 529 account is a tax-advantage college savings plan. Similar to a Roth IRA, it is an investment account that is likely to earn a higher rate of return than a savings account. 529 accounts have no income limits or annual contribution limits, and anyone can contribute.

Many of you may look at employing your child to help save for their future college expenses. A Roth IRA account can now be used for qualified educational expenses.

Above is a table comparing and contrasting some key attributes of each type of account to help you make a decision.

Conclusion

Every situation is different and there is no one-size-fits-all solution. The scenarios and content of this article may not apply to you. However, if you find yourself in the situation where you are questioning if you should make a farm purchase to offset income and lower your tax payment, you may also want to consider the option of investing in your most valuable asset – your children!

Reach out to your local GreenStone tax and accounting professional to discuss options for your individual situation or if you need assistance with any financial related services. Our team of experts is ready to help!

To view the fall 2024 issue of Partners magazine in its entirety, click here.

Fall is the spark of many things, like the leaves and weather changing, but that’s not the only thing. For many families it also means our schedules change too with school, sports, and holidays! Watching your family grow and get busy brings so much joy, but how many of us are wishing we had just that little bit of extra quality time with our family?

With full schedules it’s easy to miss out on some of the little things that can move lower on the priority list as other commitments are added on. Use these easy tips and tricks to get the family a little more intentional within our everyday lives. Whether you have littles or teenagers, these are sure to get the whole family involved!

1. Create a family calendar and find a chunk of time to go for a walk, help with homework, or even do some household chores together. It can be 20 minutes or a few hours, setting this up will give everyone something to look forward to when the schedules are hectic!

2. Watch each other’s favorite movies! With the family calendar, try to set aside an evening where you rotate whose favorite movies you watch with the family. Watching someone’s favorite movie shares a little bit about them and makes everyone feel included.

3. Screen free mealtime – dinner is definitely a good time for everyone to come together and share about their days or week! Setting up a day where everyone can be present and talk about their excitements sets up a good time to visit and be intentional with the time you share

4. Create a holiday tradition like shopping or wrapping gifts together, decorating for each of the holidays, or cooking a meal together. These all give each member of your family something to help with and can create some of the best memories!

5. Write down a couple of questions like “What was the best part of today?” or “What could have made your day better?” and set them up in a high trafficked area of your home. Every time someone goes by they can answer the questions to those in the room and start a conversation with everyone.

As schedules only get busier, we hope that your family can use these tips to increase your quality of the time you do have together. Every moment counts!

To view the fall 2024 issue of Partners magazine in its entirety, click here.

The holidays are a joyous time of the year, filled with laughter and gifts! With each gift or large family meal there comes a tradeoff, extra waste. During the holiday season plastic, food, and water waste go up drastically. In the spirit of holiday giving, what are ways we can give back to our environment during this time?

1. One of the easiest ways to better your environmental footprint is to conserve energy. Turning off lights, unplugging appliances, and getting light bulbs that save energy are all ways to shave a bit off of your electric bill, especially once family gatherings start!

2. Reduce the use of single use cutlery and plates. When getting the whole family together it can be easy to choose plastic silverware or paper plates as an option of convenience. Take the opportunity this year to choose the reusable option and reduce waste this holiday season.

3. Take leftovers from the gatherings! Food waste is almost inescapable around the holidays, but to limit that you can always take leftovers and reheat them the next day or even freeze it to save the holiday spirit!

4. Buying local products or food helps your local economy. When shopping for gifts or bringing a dish to pass, doing a simple search of locally made products near you helps the local economy and families in your community!

5. Lastly, try to conserve water. This one may be the trickiest, but most beneficial for our planet. “Trapped water” refers to water that never can go back into the environment, meaning leftover water in water bottles, coolers, or any other container. Taking the extra step to dump trapped water or even reusing pasta water for nutritious houseplant water is a great way to conserve your water usage and return water back into the environment.

Keep these eco-footprints in mind this holiday season with these tips as you have large celebrations or small family gatherings. We hope these tips are useful and you have a safe and sustainable holiday season!

To view the fall 2024 issue of Partners magazine in its entirety, click here.

Enjoy the flavors of the fall harvest with this hearty wild rice and kale bowl! Made with farm fresh produce from Sullivan Family Farm, this easy and filling dish features a variety of seasonal fruits and veggies that are as delicious as they are healthy!

Ingredients

For the Bowl:

- 5 cups chopped kale

- 1 cup of wild rice blend

- 1 Honeycrisp apple, chopped

- 3 oz of feta cheese, crumbled

- ¼ cup of dried cranberries

- ¼ cup of toasted and sliced almonds

For the White Vinaigrette Dressing:

- ¼ cup white balsamic vinegar

- ¼ cup extra virgin olive oil

- ¼ teaspoon salt

- ¼ teaspoon onion powder

- 1 teaspoon minced garlic

Instructions:

- Bring a medium-sized pot of water to a boil and add wild rice blend. Let simmer, and cook for approximately 30-35 minutes, or until rice is tender.

- Whisk together ingredients for your white vinaigrette dressing in a small bowl and set aside.

- Toast your almonds by placing them in a pan by themselves over medium heat. Toss for 4-5 minutes until they become fragrant.

- After the rice has cooled, fluff and transfer to a large mixing bowl. Add chopped kale, apple, feta cheese, dried cranberries, and toasted almonds.

- Toss with vinaigrette dressing, serve and enjoy!

Makes 2-3 servings.

To view the fall 2024 issue of Partners magazine in its entirety, click here.

Environmental regulations have a strong political component. Environmental regulations, like other policies, are reflective of the party in power.

President Trump’s Administration preferred fewer regulations and famously (or infamously depending on your viewpoint) withdrew from the Paris Climate Accord. In contrast, President Biden has expanded environmental regulations and the reach of the regulations. Early in his administration, President Biden issued an Executive Order stating climate change and environmental justice would be incorporated in all areas of the government.

This past spring, there were a flurry of final environmental regulations that reflect this view of increased regulation. The ink was barely dry on one regulation when a new one hit the printing press. The regulations were advanced rapidly because according to Thompson Reuters, “The Biden administration (was) racing to finalize a slew of major environmental regulations to help safeguard them from potential reversal should former President Donald Trump win the 2024 presidential election.”

One of those recently promulgated regulations, The Clean Water Act – Facility Response Plan is reflective of the Executive Order mentioned above. This regulation assumes increased severe weather events as a result of climate change. This climate factor requires more facilities to prepare a Facility Response Plan then would have been required without factoring in increased “weather events.” Environmental justice is mentioned more than 30 times in the final regulation.

Environmental justice has also been used to justify enforcement efforts and in some cases deny permits (and permit renewals) in certain areas of the country that have been deemed as “overburdened.”

This political component is often what adds controversy to developing regulations – they should not be so strict or they are not strict enough. As outlined below, political interests not only influence environmental regulations – but the challenge of regulations as well.

Updating PFAS Regulations

In the fall 2023 Partners, we covered the developing regulations involving per- and polyfluoroalkyl substances (PFAS). It is not hyperbole to say that these chemical compounds, which number in the thousands, are found everywhere across the globe.

The Environmental Protection Agency has recently taken several steps to regulate PFAS, part of the slew of major environmental regulations mentioned by Reuters.

First was establishing maximum contaminant levels (MCLs) for six of the PFAS chemicals under the Safe Drinking Water Act. The lowest of these MCLs is 4 parts per trillion (ppt). For perspective, a ppt is 1 second over 31,500 years.

The other final PFAS regulation is the classification of two PFAS chemicals as hazardous substances under the “Superfund Law.” This means if you have these chemicals above regulatory levels, it could result in Superfund liability. It also (potentially significantly) will affect buying and selling property, including agricultural property.

PFAS Liability

There is growing concern over the magnitude of PFAS liability, which touches nearly every business sector. Attorney Ralph DeMeo (Guilday Law) said of the PFAS liability, “There’s not enough gold in Fort Knox to pay the damages and the settlements that are gonna come out of this. There’s just literally not enough money…there is a lot of concern about bankruptcy.”

With trillions of dollars in environmental liability and the potential for bankruptcy, the domino effect could have some impact on agriculture or agricultural suppliers.

One of the biggest concerns for agriculture when it comes to PFAS is the biosolids component. We covered this in the fall 2023 issue of Partners. While we cannot predict how this will conclude – it is potentially a very big issue to monitor.

PFAS Regulations Challenged

The American Water Works Association and the Association of Metropolitan Water Agencies are challenging the PFAS in drinking water regulation. In the challenge, they state the EPA, “failed to adequately consider comments filed by the organizations and other stakeholders, and did not abide by all the requirements of the Safe Drinking Water Act during the development of the standard.” Estimates to address PFAS in drinking water are as high as $175 billion.

The Associated General Contractors of America, Inc., National Waste and Recycling Association, and the Chamber of Commerce of the United States filed a petition in the United States Court of Appeals for the District of Columbia challenging the EPA’s designation of certain PFAS as hazardous substances. They are challenging whether the EPA appropriately considered the cost before promulgating the rule.

The Chamber estimates the annual cost for compliance with the hazardous waste designation to be $700 to $900 million.

One of the critics of the PFAS standards is Susan Goldhaber (American Council on Science and Health). In 2023, Ms. Goldhaber wrote, “The extraordinarily low numbers will lead to years of litigation, unnecessary consumer fear, and billions of dollars spent on low-risk compounds.”

In a perfect world, environmental regulations are developed and implemented based on sound science and without political influence. We don’t live in a perfect world so how PFAS is resolved and the fate of the many other environmental regulations that were recently passed may rest in the courts and the elections this fall – because it’s political.

ABOUT THE AUTHOR

Alan Hahn has an undergraduate degree in Environmental Studies and completed a graduate program in Environmental Management. He has worked in environmental management for 45 years. He has written hundreds of blogs and articles. In addition to GreenStone Partners, his published work includes Progressive Dairy, Manure Manager, Michigan Lawyers Weekly, Detroiter, Michigan Forward, and HazMat Magazine.

The opinions stated herein are not necessarily those of GreenStone Farm Credit Services.

To view the fall 2024 issue of Partners magazine in its entirety, click here.

Whenever I start preparing to share another set of tech tips, I always hope it comes at a time free of alarming news about a recent security breach or some other dire cybersecurity issue.

However, like clockwork, another breach happens. So, before diving into the topic of AI and Deepfakes, let’s address the recent significant data breach.

This time, it was National Public Data, a data aggregator for background checks, which confirmed their computer systems had been compromised. The hacking group USDoD alleges to have stolen the personal records of 2.9 billion people (DeLetter, 2024). These records include name, address, and social security numbers. If you want to find out if your personal information was part of that breach the following sites can help NPD Breach Check – Pentester.com and Have I Been Pwned: Check if your email has been compromised in a data breach – now onto our regular scheduled program (topic).

A few years ago, terms like Artificial Intelligence (AI) or Large Language Model (LLM) would have been unfamiliar to many people. Unless that is you were a fan of the Terminator movies and equated AI with Skynet, but I digress. Fast-forward a few years and AI and LLM are all the rage. It seems like every new product is offering some fancy AI features, and even Apple, Microsoft and Google have introduced AI into the tools that we use every day, changing the way we use technology. While AI is not as scary as Skynet, the rapid advancements have made it easier than ever to create highly convincing fake content, and the really scary part is we are only at the infancy of these technologies.

Deepfakes are hyper-realistic videos or audio that mimic real people and even their voice. Products like ChatGPT and Microsoft CoPilot can generate human-like text which is blurring the lines between reality and fiction. While these technologies offer numerous benefits like the ability to quickly summarize information or explaining complex topics, they also pose a significant risk. Threat actors are weaponizing these AI tools to commit fraud, steal financial information, and spread misinformation.

Imagine this scenario: you receive a video call or message from someone who appears and sounds identical to your financial advisor, requesting sensitive information such as your social security number. Similarly, imagine getting an AI-generated email that lacks the typical signs of phishing, like misspellings or grammatical errors, and instructs you to transfer money to a fraudulent account. How would you evaluate and respond to these types of communications? As AI technology continues to evolve, the threats are becoming more prevalent, making it more crucial than ever to safeguard yourself.

How Deepfakes and AI Pose Risks to Your Financial Security

Threat actors are finding new ways to exploit financial services by using deepfakes and AI-generated content to impersonate trusted individuals, manipulate communications, and trick people into making harmful financial decisions. Here is how these technologies are being used to target customers like you:

- Impersonating Financial Representatives – Criminals are using deepfake technology to create highly convincing videos or phone calls that impersonate bank officials, financial advisors, or company executives. These deepfakes can be used to instruct you to transfer money, share sensitive account details, or approve financial transactions. The AI-generated content looks and sounds so real that even the most vigilant person can be deceived. In February, a multinational firm was tricked into paying out $25 million to a threat actor using this type of deepfake technology (Chen, 2024).

- Phishing Emails – Tools like ChatGPT can generate incredibly convincing phishing emails that mimic legitimate financial communications, including the nuance of someone’s tone and writing inflection. Threat actors use these emails to trick you into clicking malicious links, providing account credentials, or transferring funds to fraudulent accounts. The level of realism in these messages makes it much harder to spot the fraud. Since 2022 there has been an increase of 1,265% of malicious phishing emails, and a rise of 967% in credential phishing (Violino, 2023).

- Identity Theft Through AI – Deepfakes and AI-generated content can also be used to steal your identity by creating fake videos or audio of you interacting with financial institutions. There have been examples where hacking organizations have been able to successfully steal biometric data. These forged interactions can be used to open new accounts in your name, apply for loans, or authorize fraudulent transactions, all without your knowledge.

Steps to Help Safeguard Against Deepfakes and AI Risks

As these risks continue to advance, it is essential to adopt stronger cybersecurity practices to protect your personal financial information. Here are specific steps you can take to safeguard your accounts and financial assets from AI-enabled fraud:

- Verify Requests for Financial Information – Always be cautious when receiving requests for sensitive financial information, especially if they come through unexpected channels like email or video calls. GreenStone will never ask you to reply to an email message to update your confidential information or to provide a PIN, account number, social security number, username, password, or other similar information. We recommend to our customers never to respond to any email or call that asks for such information, even if it appears to be from GreenStone or another financial institution. If you are unsure of the authenticity of a communication, contact us to confirm. If you suspect fraud has occurred in connection with your GreenStone accounts, please let us know immediately and we will promptly assist you in resolving the matter.

- Use Strong Authentication Methods – If you could do one thing today to protect your personal financial information, it would be enabling multi-factor authentication (MFA) everywhere you can, including email, online banking and financial accounts. Our customer portal, My Access, offers MFA by sending a code via text or a phone call to your device to verify it’s you. MFA adds an extra layer of security by requiring a second form of identification beyond your password, such as a code sent to your phone or email. MFA can help prevent unauthorized access, even if your login credentials are compromised.

- Stay Skeptical of Unusual or High-Pressure Requests – Threat actors often create a sense of urgency to trick you into making quick decisions. Be wary of any financial communication that pressures you to act immediately, especially if it involves transferring money or disclosing sensitive information. Take the time to double-check and verify the request. Trust but verify!

- Monitor Your Financial Accounts Regularly- Keep a close eye on your bank statements, credit card transactions, and investment accounts for any unusual activity. Set up account alerts to notify you of suspicious transactions, withdrawals, or changes to your account information. Additionally, putting a freeze on your credit file prohibits consumer reporting agencies from releasing your credit report without your express authorization. Protecting Your Information | GreenStone FCS

With the advancement of deepfake and AI technologies, the threats to financial security are increasingly significant. Threat actors are using these tools to generate believable counterfeit communications, impersonate reputable financial officials, and deceive customers into disclosing sensitive data or approving fraudulent activities.

Protecting your personal financial information and assets from the new surge of AI-driven fraud involves staying informed, implementing robust cybersecurity measures, and verifying any suspicious financial requests.

To view the fall 2024 issue of Partners magazine in its entirety, click here.

What’s a way to get even more out of your hunting land? Buy it with friends or family!

While making a purchase with other people has its own set of challenges, you can avoid many of the pitfalls and only realize benefits by keeping these tips in mind:

Set up an LLC

When it comes to financing, setting up an LLC makes it easier to work with your lender. For instance, if you have ten people involved in an LLC, you don’t have to have all ten apply for a loan. Instead, you can take just one or two people who have good credit and cash flow, and the lender can work with those applicants. GreenStone is able to make the entire process simpler for groups seeking financing.

Discuss your goals and management plans

Owning property comes with many options, and having answers to some common questions can simplify it. Who will be involved in decision making? What will you do with the land? Will everyone use it at the same time or different times? It is also important to discuss if you will improve the land, and if so, how you will pay for it. Discussing these factors ahead of time can help set you up for success in the future and avoid difficult conversations later.

Come up with a workable budget

It is easier to buy more land if you’re pooling resources, but everyone needs to know where to start. Is every party putting in the same amount of money? Who’s responsible for paying the tax bill? Are there buildings on the property that require dollars for upkeep? Will there be attorney costs?

Taking time to talk about these issues keeps everyone apprised of the financial impact of owning recreational land. This way, if the property seems out of reach for some members of the group, they’ll be able to decide ahead of time, not later when they’ve already made the investment. Of course, friendships are more valuable than hunting land, so be certain that all the information is on the table before proceeding. For this to be successful, everyone needs to be open about their personal financial budget.

Establish a “Slush” Fund for Maintenance or Improvements, Taxes, and Other Incidentals

Like owning any property, particularly if there is a house or building on it, funds will be needed for maintenance, improvements, taxes and other costs associated with the property. Determining a monthly amount for each member to contribute provides the money necessary for ongoing expenses. Many groups will create a designated account to hold these funds to make loan payments and cover other expenses.

Talk schedules

We’ve all heard about problems with shared vacation homes that you do not want to experience! Avoid arguments about which hunter got the most deer and what’s fair by making certain you are buying with people who agree on when and what land use is allowed. Can everyone go at the same time at the beginning of hunting season? Is it okay if some people go more than others? Are guests allowed? Discuss all the issues before purchase, so by the time it’s hunting season everyone knows where they stand.

Discuss long term plans and potential conflicts

Sadly, life events happen such as death, divorce, or job loss, and new life chapters take place like marriage or geographic moves. All of these changes can complicate land ownership. It is also difficult to transition land ownership generationally when there are multiple parties involved. However, these issues can be tempered by the positives of requiring less individual money to own land, making your own rules, and sharing costs so you can own a piece of paradise to share with your friends and family.

By keeping these few tips in mind, it will make the transition of buying group hunting land a little smoother.

And when it comes to financing, visit your local branch to speak with a financial services officer and start working toward your dreams today!

One on one relationships are key in personal relationships, but what about as a consumer? What if you were able to have a one-on-one relationship with the people growing and producing your products. That is a large part of Dandan Zhu’s operation. She and her husband, Adam, self-distribute all of their products to keep the one-on-one relationship with their customers.

The Zhu’s family operation consists of beef, pork, lamb, chickens, ducks, goats, turkeys, eggs, and flowers by season! Dana says they want “to show that a mid-scale, multi-species farm can be viable.” They first bought the farm in 2019, and in 2021 they started selling meat. When they bought the land, it had been fallow for 5-10 years and needed major improvements before being planted, but little by little they have been accomplishing their goals.

To continue to grow their operation, this year Dandan used the CultivateGrowth grant to attend the Make It In Michigan Seminar. This seminar is an MSU Sponsored conference for Michigan small scale food producers to network and meet distributors. When asked her favorite part it was “Meeting with passionate makers of specialty foods from the state. We have added a number the products of several other producers to our farm store.”

Their overall goals are “To be the trusted supplier of regeneratively produced animal proteins in northwest lower Michigan.” Regenerative agriculture is a food production system that uses and reuses farm resources to restore soil health, support the climate, water resources and biodiversity. Practices like cover crop rotation, keeping roots in the soil, rotational grazing, and using natural compost or animal byproducts to spread on soil allow them to waste less and utilize more opportunities in their farm.

The CultivateGrowth grant has allowed Dandan to realize how important it is to her to self-distribute their products and build that relationship with those around her. GreenStoneunderstands the importance of supporting education for young, beginning, and small farmers like Dandan. We work to provide the educational and financial resources needed to help establish a solid foundation. To apply for a grant, visit CultivateGrowth Grant.

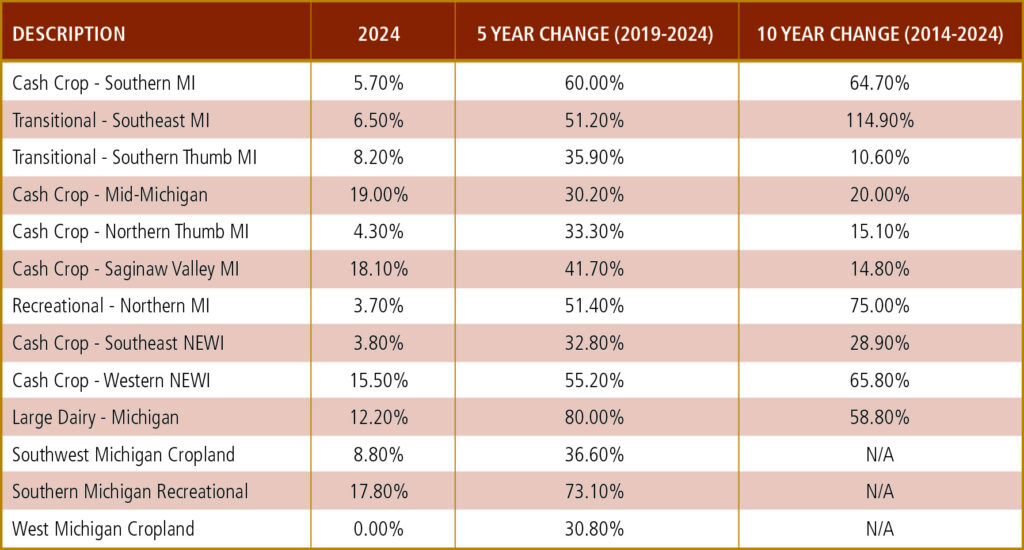

How Land Value Benchmarks are Determined

Every year, annual land value trends are observed by GreenStone Farm Credit’s team of expert appraisers. These trends are measured by re-appraising the same thirteen plots of land representing unique market areas in Michigan and northeast Wisconsin. GreenStone evaluates these properties annually to give landowners and customers a picture of how the value of cropland, transitional land, recreational land, and dairy improvements have changed throughout the past year. Factors such as commodity prices, governmental regulation, tourism, and weather all help determine the market value of land within these regions. Reevaluating the same plots of land every year also eliminates any variance that could occur with other survey methods, leading our appraisals to the best representation of market value trends.

The Results are In

Overall, the results across all thirteen benchmarks grew again this year as you can see in the table below. For the fourth year in a row, land values only increased, ranging from a 3.7% increase all the way to 19%. For landowners, these results ring positive, but for those looking to acquire land, these rising prices continue to present challenges. Many aspiring landowners are now facing all-time-high land prices coupled with challenging commodity price outlooks. Despite these realities, demand for land remains high and inventory is scarce. With this competitive environment, it’s easy to see why we’re noting significant positive gains in value across the board for all thirteen land benchmarks.

Dairy and Cash Crop Summary

In 2023, our value benchmark representing a CAFO sized dairy operation saw a historic year-over-year increase in value due to rising construction costs and a thriving dairy market. That trend somewhat moderated but continued into 2024 with a 12.2% increase in value for large dairy operations in Michigan and Wisconsin. As this trend is heavily influenced by construction costs, the benchmark has nearly doubled in value over the past four years.

Land benchmarks for cash crops continued to hold steady in the northeastern Wisconsin region with a year-over year increase of 3.8%. The western part of northeast Wisconsin saw another spike in land value due to rising competition for limited land. This trend has been constant in the region over the past several years and appears it will remain the same going forward. In keeping with the trend, all Michigan cash crop value benchmarks also experienced steady increases in value.

Recreational and Transitional Summary

Recreational land and transitional land (agricultural land expected to be developed into another use in the future), continued to experience increases in value. However, that increase was not as significant as it has been in years prior. The period directly following the COVID-19 pandemic showed a widespread movement of people leaving urban areas to more rural destinations or purchasing recreational land. That trend seems to be leveling off, as the value of these land types has become more moderate in the past year. This trend can be seen across the land benchmarks in Michigan’s southeast and southern thumb regions, and northern Michigan. Increased interest rates, inflation, and other economic factors all play a role in the decreasing strength of land values.

It’s Still a Good Time to Own Land!

An unwavering fact from this year’s land benchmark results is the value of land continues to increase, and the good news for landowners is it’s very likely the value of your land has increased over the past year. Buying land continues to be a strong investment for your future!

GreenStone’s team of financial experts can help find a unique solution that’s tailored to you, whether that’s helping you secure your dream plot of vacant land or expanding your farming operation. Click here to learn more about the resources GreenStone provides when it comes to purchasing land.

This blog was originally published in Michigan Farm News.