After a cold and snowy December morning of deer hunting, Daniel Krug joins his wife Jennifer to enjoy a cup of coffee by the warmth of their fireplace in their newly-built barndominium-style home.

It’s the kind of peace and quiet you can only get on the backroads of Holly, Michigan. Although originally hesitant to move to such a large plot of land, coming from living in the suburbs, Jennifer now appreciates this newfound serenity.

“It was during COVID and the lockdowns when we decided we didn’t want to be in the suburban areas anymore,” Jennifer explained. “I wanted to downsize our home now that we are empty nesters, but I knew Dan’s dream was 40 acres.”

That 40-acre dream turned into a 65-acre reality after Daniel and Jennifer toured the plot of land they now call home.

“When I first heard 65 acres, I was wondering who needed that much. Now, I realize I like it. There’s nice trails to walk through the woods. I feel like I’ve visited all corners of the properties,” said Jennifer.

The two worked with GreenStone Financial Services Officer Miranda Kelle to secure a land loan and buy the property. Soon after, they called up Miranda again to finance a home construction.

“Everybody was awesome at GreenStone. We were happy to work with a local lender who understands exactly what we want,” said Jennifer. “Our builders loved working with GreenStone, too. It was a natural choice to go with GreenStone.”

“With it being a unique type of build and the size of the property, we knew it was up our alley to finance it,” explained Miranda.

By August 2022, their two builders broke ground on the home while Daniel and Jennifer lived in a temporary building on the property they refer to as the “glamping tent.”

After a cozy full year in the small structure, Daniel and Jennifer, along with their two dogs Ziva and Ellie, were finally able to move into their new, state-of-the-art barndominium – even hosting a large Thanksgiving for family this past November.

“Daniel told me that Thanksgiving in the new house was amazing,” said Miranda. “That meant a lot to me because it’s a great example of the meaning of our job. We get to help make those big moments happen.”

“It’s nice to have the kids and grandkids here,” Daniel explained. “Everyone felt at home by the end of the day Thanksgiving.”

It’s difficult not to feel a sense of home in their cozy rural setting. The home is equipped with a large kitchen, 2540-square-foot garage, and plenty of living space for their seven grandchildren to enjoy.

“I like the open design and the big fireplace,” Daniel pointed out.

“The vaulted ceiling and the beams in the ceiling were things I always wanted,” Jennifer reflected. “The big island and large pantry are also very cool for me.”

There are even some personal touches that remind Daniel and Jennifer of friendships they have developed along the way.

“We had a friend that had a milking barn that unfortunately was flattened in a storm,” Daniel said. “We bought the wood and used it for a beam in the kitchen, the fireplace mantle and two vanities.”

Daniel and Jennifer say it didn’t take long to adjust to the lifestyle change from the city to the country.

“I used to have a suit and a BMW, and now I have a cowboy hat and a truck,” Daniel joked.

“I would just tell anyone that if they are looking for a switch in lifestyle, it’s a lot of work but it’s very rewarding,” said Jennifer.

The home build may be complete, but they are just getting started on this property. Next on their agenda: raise some horses.

“We have an equestrian barn to put together,” said Daniel.

If anyone knows how to take a big idea and turn it into reality, it’s certainly Daniel and Jennifer, and the team at GreenStone will be there every step of the way.

“It’s exciting to see what else they can do, especially with this size of property,” said Miranda. “We keep the relationship open and wherever their ideas go, we know we are a resource for them.”

In the meantime, they will continue enjoying fresh coffee, the fireside ambiance, and the endless possibilities of this new home and lifestyle.

“One of my favorite parts of the job is being able to see people’s dreams come to life and being able to help them do that,” said Miranda. “This isn’t just about financials, it’s about getting people in their dream home.”

“I do believe that God led us here, and I know God is going to continue to provide as long as we follow Him,” said Jennifer.

To view the winter 2024 issue of Partners magazine in its entirety, click here.

Geert Van den Goor has been measuring in acres instead of miles for as long as he can remember. Growing up on a farm in the Netherlands, agriculture has always been in his blood, and when he graduated from school in 1983, he pursued that passion and began farming with his brother.

Eighteen years later, Geert and his wife Gertie were looking for more opportunities to expand their farming operation, and when country regulations got in the way, they decided to move to the United States. There, Goma Dairy Farms was born in Marlette, Michigan.

If you visit their property now, you will find a wide-scale dairy operation, but it hasn’t always been this way.

“We started in 1999 with 250 cows and 350 acres,” Geert reflected. “By the second year, we built a new barn for 600 cows.”

And by 2006, Geert and Gertie had a brand-new parlor. As the years went on, the farm grew to 3,500 cows.

A New Direction

Knowing their three children were not taking over the farm upon their eventual retirement, in 2015 Geert and Gertie began to evaluate the future of Goma Dairy Farms.

Brent Robinson, a dairy farmer in neighboring town Caro, Michigan, worked as a nutritionist on Goma Dairy Farms in the past, and formed a friendship with Geert and Gertie. When he found that they were searching for the future operator of their farm, he threw out the idea for himself, along with his business partner, Brent Moyer, to eventually take it over.

“One weekend we were out around the campfire, and Brent asked if we had ever thought of them,” Geert recalled. “Two years later, we put a plan together on how we were going to do it.”

By 2019, Brent and Brent’s farm, Paramount Enterprises Dairy merged with Goma Dairy to be known publicly as Green Point Dairy.

Geert says the secret to the success is leaning on everyone’s individual expertise.

“Everybody respects the qualities of each other,” said Geert. “We use each other’s qualities very wisely.”

GreenStone VP of Agribusiness Lending Tara Parr, who has been instrumental in the financial side of the merger, couldn’t agree more.

“Geert and Gertie are very proactive and good decision makers, and Brent and Brent are a breath of fresh air,” said Tara. “The merging of the two companies was pretty seamless.”

Going Green

One of the largest decisions made by Green Point Dairy was the addition of an anaerobic digester on the farm’s Marlette, Michigan property. Energy companies SJI and REV LNG installed and run the digester that turns cow manure into methane gas.

“The company showed up, and it was the first time a salesperson talked a normal language and had something we actually wanted to learn more about,” Geert explained.

The addition of the digester comes after the farm already installed a machine that separates manure from the sand used for the cow’s bedding. It also cleans the sand to be continually reused for the cows. This machine paved the way for the digester – because manure cannot be turned into gas unless the sand is first removed.

Geert and Gertie, along with Brent and Brent, believe that a step toward sustainable farm practices is beneficial for everyone.

“The future of agriculture is going to revolve and evolve around sustainability,” explained Brent Robinson. “Creating a new system that functions with business models and biological models working together to create an ecosystem that can work long-term for the planet and people are the first steps toward this.”

Recently, GreenStone President and CEO Travis Jones, joined other members of GreenStone’s staff on a visit to the farm to check out the sand separating machine and the digester to learn more about how they work.

“It says a lot about GreenStone that Travis visits these operations,” said Tara. “He wants to be involved at all levels.”

This visit was especially special for Geert and Gertie, who have worked with GreenStone since they came to the United States almost 25 years ago.

“It was exciting that the CEO was interested in visiting us,” said Geert.

Sitting around the table with hot coffee topped off with farm-fresh milk in hand, Geert explained that GreenStone has helped on a number of projects and expansions over the years, and he’s thankful for the rural-focus of the cooperative.

“In 2005, when we did a big expansion, we got the best package for what we needed with GreenStone,” said Geert. “We have a lot of qualified people around us at GreenStone.”

For GreenStone employees like Tara, it’s just another day doing what she loves – supporting agriculture.

“The best part of my job is the people. I get to build a lot of relationships,” Tara explained. “This is not a transactional business. Understanding the business and family dynamics is all part of building that relationship.”

Moving Forward

Brent and Brent’s plans for the future of Green Point Dairy are already underway with the construction of a state-of-the-art heifer facility. Once finished, it will be able to house heifers, securing a successful future for the farm – allowing Geert and Gertie to rest easier knowing as they inch closer to retirement, the future is bright for the operation they helped build.

As the years go on, GreenStone will be there to support what’s in store.

To view the article in the online 2024 Winter Partners Magazine, click here.

Steve and Lynette Henson bought an Amish farm in Blanchard, Michigan back in 1998 with one goal in mind: enjoy the peace and serenity of living in the country.

What they didn’t expect is that the farm would give them a brand-new hobby-turned-booming business.

The farm’s former resident left tree tapping supplies behind, so when Steve and Lynette moved in and got settled, they gave it a go, and loved it! Soon, they began producing more and more maple syrup – eventually deciding to sell it.

“It was kind of a hobby at first, and then we enjoyed making it and had fun,” said Lynette. “There were a lot of maple syrup producers around us when we started, so there wasn’t a huge market. We had to go to Detroit to sell our products.”

Fast forward to more than 25 years later, and their business, Doodle’s Sugarbush, LLC, has taken the market by storm. You can find their syrup in more than 200 grocery stores and restaurants across the state and country – something that took years of hard work and networking to accomplish.

“You have to get in front of these stores for them to believe in your product,” said Steve. “It can be hard to do.”

Doodle’s Sugarbush, LLC isn’t just known for their wide variety of syrups, but also maple-based products like maple cream, maple coffee and maple pancake mixes.

“Mostly everything we do is made from maple syrup,” Lynette explained. “Maple syrup is a healthy sweetener; it’s a good sugar source. As we’ve grown through the years, we just keep expanding and adding more products. There’s lots of things that you can make with maple syrup.”

The operation is difficult to forget – not only from its unique product line, but from its memorable name as well.

“Doodle is Steve’s childhood nickname,” explained Lynette. “We decided to go with it for our business name to honor that.”

It’s so memorable that they often see different generations of families stop by to support the business.

“I take great pride in selling to people in the community, and then years later, selling to their kids and grandkids. We get to see families from the past.”

And GreenStone takes pride in being a part of their team, as well. Steve and Lynette have been able to utilize farm real estate loans, operating loans and equipment loans through GreenStone to help in the expansion of their business.

“Traditional banks hadn’t always wanted to give us a loan for a maple syrup farm,” said Lynette. “GreenStone took us seriously and knew we had a full-fledged business. GreenStone has been really great to work with to help us pursue our dream of helping make it bigger and better.”

GreenStone Financial Services Officer John Grassley works with Doodle’s to find finance options to help grow the business – something that excites him.

“They have been great to work with,” said John. “They have a passion for their business, and you can tell that when you meet them. They put their all into their products, and they’re loving what they do. They’re taking something from nature and turning it into a product. It’s a unique product, and you can see it and taste it right at their farm.”

Tasting that product is what the community will continue to do as Doodle’s makes improvements to their facility and pushes out more products.

“It feels really good to help them achieve their goals,” said John. “They want to continue to be more efficient. They just set up a new packaging line that will help them achieve that.”

“There’s a huge market now,” said Lynette. “People love to support local and support Michigan.”

As far as the future, this hardworking duo has no plans to slow down any time soon. With the support of their daughter Eliazbeth who helps when she’s home from college, there’s no limit to how much success they can tap into.

“We hope to continue to increase our products and continue to grow. We hope to keep reaching out further from Michigan and across the United States,” said Steve.

“As a husband and wife operation, it’s awesome to see the family dynamic and the dedication that they have,” said John.

To view the winter 2024 issue of Partners magazine in its entirety, click here.

Deer camp. Those are two words that can lite a fire in many Michigan hunters of a certain age. What age you may ask? Good question. I have given that quite a bit of thought over the last several years.

My dad, who is now 80, is still drawn by the allure of deer camp. The sad fact is, physically he can’t navigate getting to and from deer camp on his own any longer. A stroke robbed him of that gift several years ago, but the spark and the memories still smolder. The question is, are the traditions of deer hunting being passed down? Is deer camp still a thing? Well, the answer is a resounding yes…and no.

I have the extreme honor of having the job as host of Michigan Out of Doors TV. That little camera has given me a pass into many deer camps around our great state over my 26 years of working for the show. I have been to many a cabin, tent, house, camper, home and hotel all doing their part to host a deer camp. At every camp, it seems like there’s a couple of different age classes of hunters, starting with the old guard.

By that I mean, folks in their 60s, 70s, and 80s. They tell the best stories, and if you’re lucky enough to go back year after year, the stories usually get better and better over time. These guys still like to hunt, but aren’t too concerned about filling a tag. They’re still the first ones up, but not usually the first ones out the door.

Then there’s the guys in there 30s, 40s, and 50s. Some are still pretty hard core, hunt hard, and are very into all that goes into the hunt. They run a ton of trail cams, have full scent control, and can name all the bucks on their property. However, many in this age range have started to transition to a bit more of a casual hunter. They only sit until 10 or so, don’t scout much, don’t know what grain bullet they shoot, and they are more into what the dinner plan is then who is sitting in what blind.

Then we have the up-and-coming hunters, the young ones. It’s these that I am worried about, and I have two of them in my own house. For some of them, they have gotten bit by the hunting bug and can’t wait to hit the woods! They love the allure of the outdoors. They love hunting deer, ducks, big bass, or whatever else they can chase! These young hunters will hopefully take our sport into the future. There are also many, like my two boys, who each shot a few deer and really like it but haven’t fallen in love with it yet. They will always support it, will go from time to time, but haven’t yet made it a priority in their lives.

Deer camp is the place that all of these folks can and should come together. The teenager, the hardcore 30 year old, the casual hunting 45 year old, and the 70 year old story teller. If our sport is to grow, and thrive, I believe that keeping deer camps part of the hunting landscape is crucial. The memories, the stories, and the deer on the pole are all an important part of making the tradition of deer hunting continue. The world would be a better place if we all went to deer camp.

To view the winter 2024 issue of Partners magazine in its entirety, click here.

Timber is a different business than any other. Timber professionals need to purchase before they make a profit, their equipment depreciates at a rapid rate, and every step has to be done keeping the health of the regenerative product in mind. GreenStone recognized this, dove in and learned it, and now has a long history of working in this industry. As a result, we understand the specific needs for operating loans, equipment loans, leases, mortgages, and letters of credit.

Application process

One of the biggest questions prospective members have is about the application process. Most of the time, timber financing deals require traditional underwriting, three years of complete tax returns, and a complete balance sheet. For new prospects, we have found it beneficial to them to walk them through all the documentation that is needed.

At GreenStone we’re able to do this both virtually and in person. We know this is a detailed process, particularly for new members. We help them through the application, which helps them understand why things are needed and makes it easier to know what to expect the next time they apply. There are five main items applicants need:

- Certificate of Authorized Representative (for borrowers with legal entities)

- Signed and dated application

- Copies of drivers’ licenses

- Three years of Federal and State Tax Returns along with depreciation schedules

- A complete market-based balance sheet for all entities and individuals co-signing or guaranteeing the loan(s)

Underwriting and depreciation

Customers also want to know about GreenStone’s underwriting standards and how depreciation plays into them. Due to the intense wear and tear timber equipment experiences, it depreciates more quickly than standard farm equipment. For example, in a matter of three years, a piece of equipment can go from being worth $700,000 to $375,000. Since we’re familiar with the intense replacement schedule loggers are on, we like to work with our customers to make the best choices on financing equipment – whether it be regarding term of loans or down payment.

GreenStone has four core underwriting standards as it pertains to timber:

- Repayment history (captured by credit bureau details)

- Owner equity

- Repayment capacity

- LTV (loan-to-appraised value)

For young or beginning operators, GreenStone also has more flexible standards to accommodate those who we see as the lifeblood of the industry moving forward.

Letters of credit

Timber operators commonly are asked to put up a cash bond on sales before they cut the wood on the property, and many don’t want to tie their cash up in those deals. To assist them, a timber operator can pledge collateral, and GreenStone will write them a letter of credit. This is a service we provide that differentiates us from many other financial institutions. As a bonus, our Irrevocable Letters of Credit do not typically accrue interest, can be originated with a reasonable fee, can be written for up to seven years, and are renewable. Many of our timber customers use them and like the business opportunities they afford them by preserving their cash position.

Real estate

Timber operators buy land with the purpose of harvesting the timber. When they require financing for the purchase, GreenStone requires 65% LTV on vacant timberland as we expect borrowers to select-cut the property at some point during the course of the note and we want to protect their equity position as well as GreenStone’s collateral position. In many circumstances, members will resell the land after a cut and regrowth period as either recreational land (e.g., for hunting) or as residential property tracts for rural homes. This practice – if done responsibly – is both a good way to maintain healthy forests and promote tourism and rural living across GreenStone’s territory.

Sustainable Forestry Initiative (SFI) Training

Timber professionals must complete eight hour of SFI training to satisfy wood-procurement and harvesting requirements of many SFI-certified wood purchasing companies. The training covers Fiber Sourcing Standards, MIOSHA Safety, Best Management Practices, climate adaptation, Invasive species ID and control and more.

Searching for a new home or piece of recreational land can be exciting, but before you sign on the dotted line, it’s important to know that just because you qualify for a certain loan amount doesn’t necessarily mean it’s right for your budget. Here’s some advice to help you determine the loan amount that works for you.

The Pre-Qualification Mortgage Process

When our team works with the customer on a loan, we evaluate a borrower’s total income and any debt they have, the insurance they may have to pay on the new home and any property taxes they may take on before determining how much you could qualify for. This does not take into account every single bill you have to pay like your internet, cell phone, gas, or utility bill. That’s why it’s so important to know your own budget.

Managing Your Budget

Figuring out if you can take on the monthly payment of a new loan is on you, the borrower, but there is plenty of support to help you make an informed decision about your finances.

You can use online tools, or just do it the ol’ fashioned way: take a pad of paper and list all of your monthly bills out (and don’t forget things like gas expenses and groceries), and subtract them from your monthly income. After you see how much is left over, see how much more you can give each month towards a loan while saving enough for an emergency fund. With both pieces of financial information in mind, our team will work with you to adjust your loan from the pre-qualified mortgage amount if necessary to best fit your individual scenario.

Other things to consider with the pre-qualification of your loan

If you are currently renting or own a home, think about your current rental expense or mortgage payment. If your pre-qualification mortgage payment is similar to your current monthly payment, it more than likely fits within your current budget, unless your ultimate goal is to reduce your monthly living expense. Also, if you are renting, there are other expenses that come with owning a home. These include property taxes, homeowner’s insurance and home repairs. You can read more about these costs to consider in this article.

Another thing to think about is long-term financials. Your pre-qualification is based off your current income and debts. Be sure to consider any future financial changes that may impact your repayment capability.

Ask For Help

Figuring out your budget and what you can actually afford can be tough. Before you accept a loan, talk to the financial service officer and discuss your questions and concerns! Our team of industry experts are happy to walk through your budget to help you figure out what the best option is for your situation. Remember, just because you qualify doesn’t mean you should spend that amount, you can always adjust your loan to a lower amount you feel most comfortable with.

When it comes to choosing the right lender for your needs, consider these loan details for pre-qualified mortgages outlined here in this article.

As the year comes to a close, it’s the perfect time to start setting goals for the new year. If one of those goals is adding to your key ring and purchasing a new home, there are some things you need to take a look at, and some habits to start building.

Look at Your Debt

There are two main things a lender will look at when deciding whether to approve your loan request: your gross income and your debt ratio. The debt ratio is calculated by adding up all debt that shows up on your credit report along with any taxes and insurance on real property and dividing it by your income. GreenStone requires a debt ratio of 40% or less. That’s why it is so important to know how much debt you have outstanding on your credit report and how much any real estate taxes and property insurance may be so you can determine if it’s a feasible time to take on more debt, and if you will qualify for a mortgage loan.

To figure out how much debt you have accrued, you can download your report from each of the three credit bureaus for free once a year at https://www.annualcreditreport.com/index.action. We recommend downloading a report from one bureau every four months, as opposed to downloading all three at once. This allows you to monitor your credit and open accounts throughout the year to make sure there are no surprises at year-end.

If your debt ratio isn’t favorable and could be worked on before applying for a loan, make that a goal for the new year. Set aside money from each paycheck to chip away at your current debts before taking on more.

Evaluate your Savings

When buying a home, you will need a down payment to secure a loan. If you are able to put down 20% or more to your lender for a primary residence, you can avoid paying Private Mortgage Insurance, or PMI. PMI is required by almost all lenders if you are putting less than 20% down minimum on a primary residence purchase. If you are unable to provide a 20% down payment at signing, you will need to tack on the expense of PMI, which can be up to a couple hundred dollars per month additional on your monthly mortgage payment.

The easiest way to start building your savings for that down payment is simply by paying yourself first. Determine how much you can afford to pay yourself from each paycheck, put that money aside in a separate bank account you don’t regularly access every time you are paid, and do your best not to withdraw funds from it. For example, if you know you need $12,000 by the end of the year to secure a loan the following year, and you’re paid bi-weekly, put about $462 away each paycheck into that separate account.

It’s also a good idea to deposit any additional income you may get into that account including gift money, cash from a side hustle and bonuses from work. The faster you get to your savings goal, the faster you will be unlocking the front door to your dream home.

It’s important to note: PMI is not available for secondary residences and recreational land. If you plan to make this type of purchase, you will need the full down payment of 20% minimum in full no matter what.

Other Things to Consider

As you plan for the exciting step of acquiring a new home, before you book the moving truck, there are some other things to think about and plan for:

- If you’re currently renting, you should know that just because you are paying $1,500 a month in rent does not mean you will automatically qualify for a $1,500 house payment. That’s because mortgages are regulated by the federal government, and rent prices are not. All federally regulated lenders are required to run an affordability test for mortgage payments when you are purchasing a home. Landlords are not required to go through an affordability test for rent.

- There are additional costs to add into your future budget on top of your house payment, like homeowners’ insurance and real estate taxes. Read more about the costs of owning a home in this article.

- There are creative ways to save extra cash to get you closer to your savings goals, including no-spend months. Read some of those strategies in this article.

- Talking to a lender, even before you’re ready to apply for a loan, is a helpful step to set expectations for yourself and plan for your goals.

Your Future Starts Now

GreenStone is here to help you strategize for your long-term ideas and goals. Reach out to your local branch to get connected with one of our experienced and knowledgeable financial services officers. They can take a look at your individual situation, walk you through what to expect from the loan application process, and let you know what to have ready for submitting a loan request.

As you prepare for the end of the year, there’s an IRS change that we want to make you aware of that may impact you when it comes time to prepare your 2023 year-end forms. The IRS has lowered the threshold by which it mandates you to file year-end forms electronically to a total of 10. This change has implications for employers and taxpayers, as it affects the way tax-related information is submitted to the IRS. This message summarizes the amendment and lays out what you need to do going forward if you will have more than 10 forms this year and prepare your own year-end forms.

What changed?

On February 23, 2023, the Treasury Department issued Treasury Decision 9972, amending Regulations Section 301.6011-2. This amendment specifically targets the threshold for electronic filing of information returns—once a business exceeds a certain number of returns, the business is required to file the returns electronically. The new threshold is now 10 returns. The new threshold goes into effect next year, which means that tax year 2023 will fall under the new rules—some of which are required to be filed no later than January 31, 2024.

Why is it changing?

The IRS has given the following reasons for the change:

- Enhanced Efficiency: Electronic filing is far more efficient and less prone to errors than paper-based filing. Lowering the threshold encourages employers to utilize electronic filing, thus contributing to smoother tax processing.

- Cost Reduction: Electronic filing can be more cost-effective for employers in the long run, eliminating the need for paper forms, postage, and manual data entry.

- Reduced Environmental Impact: Encouraging electronic filing aligns with efforts to reduce paper waste and promote environmentally friendly practices.

- Timely Filing: The amendment ensures that information returns for tax year 2023, specifically Forms W-2, are filed electronically by January 31, 2024, allowing for timely and accurate processing.

Not that this will be fun for those of you impacted by it and now required to e-file forms when you have not in the past – but at least you know why the IRS is making these changes.

What forms are affected by these changes?

The following returns fall under this new threshold:

- Forms W-2,

- All 1099 Forms, including but not limited to NEC & MISC

- Form 1042-S

- The Form 1094 series

- Form 1095-B & C

- Form 1097-BTC

- Form 1098, C, E, Q & T

- Form 3921

- Form 3922

- The Form 5498 series

- Form 8027

- Form W-2G

Filers should add together any of the above forms they need to file and if it exceeds 10, they are required to file all forms electronically!

How do I get my forms e-filed?

You always have options – when the IRS enacted this amendment, they created a free portal for businesses and individuals to E-file these returns called IRIS. This website summarizes much of what is in this message and talks about the steps to be completed to be enrolled as an IRIS user.

It should be noted that you will need to get an EIN – you cannot use an SSN when using IRIS. Obtaining an EIN is quick and easy. You also need to file for an IRIS Transmitter Control Code (TCC). This apparently can take up to 45 days – we’re hopeful the IRS will process these applications quicker. The provided links walk you through the entire process.

If all of this seems all too overwhelming, contact your CPA or a local GreenStone tax accountant. GreenStone offers a full array of accounting services for farmers and other business owners and are ready to assist you with your year-end reporting needs!

During a ceremony at GreenStone’s headquarters, the AgriBank District Farm Credit Council (ADFCC) presented its 2023 Friend of Farm Credit Award to U.S. Sen. Debbie Stabenow of Michigan. Stabenow, Chairwoman of the Senate Committee on Agriculture, Nutrition and Forestry, received the award for her distinguished leadership in Congress in helping to ensure that agriculture and rural communities across the country can continue to thrive.

“It goes without saying that Chairwoman Stabenow has been a leading voice for farmers, ranchers, and rural America, and for that we owe a debt of gratitude,” said Jed Welder, a farmer from Montcalm County, Mich., and GreenStone Farm Credit Services board representative on the ADFCC. “We also are grateful for the strong, steadfast support she has demonstrated for the Farm Credit mission. She is leaving a legacy that agriculture and rural America will benefit from well into the future. We are honored to celebrate her as an AgriBank District Farm Credit Council Friend of Farm Credit and a friend of agriculture and rural America.”

To honor the senator’s long dedication to advocating for agriculture and America’s rural communities, GreenStone partnered with a number of agricultural organizations to donate $5,000 to both the Michigan FFA and Michigan 4-H in Senator Stabenow’s name.

“Senator Stabenow has been a fierce supporter of agriculture in the senate for years and has been instrumental in making sure Michigan is a central focus in the Farm Bill,” said GreenStone President and CEO Travis Jones. “We are proud to present not only this award to her, but also these donations in her name to help equip the next generation of farmers with the tools they need to thrive.”

“I’ve always had three goals for the Farm Bill: keep farmers farming, keep families fed, and keep rural communities strong. Farm Credit is about all of that. The role of Farm Credit cannot be replaced, and it’s incredibly important,” Senator Stabenow remarked. “I’ve said it a thousand times: You don’t have an economy unless someone grows something and unless somebody makes something, and that’s what we do in Michigan.”

GreenStone Farm Credit Services is one of the local Farm Credit Associations that comprise the AgriBank District along with AgriBank. The ADFCC represents Farm Credit farmers and ranchers in a 15-state area from Wyoming to Ohio and Minnesota to Arkansas. About half the nation’s cropland is located within the AgriBank District.

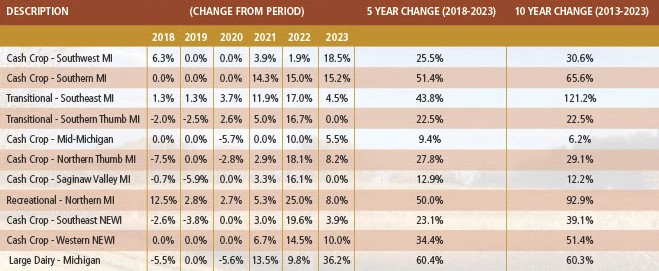

GreenStone’s appraisal team has completed a yearly land benchmark study, and the results ring positive for land owners in Michigan and northeast Wisconsin. Each year, GreenStone re-appraises the same eleven parcels of land representing local market areas across the geography. These re-appraisals are then compared to the prior year appraisals to understand value trends in cropland, transitional land, recreational land and dairy improvements.

For the third year in a row, none of the eleven parcels of land we measure saw a decrease in value as outlined below.

How GreenStone Determines Land Trends

As a part of this annual evaluation, research is also done to understand why these values are increasing or decreasing. A rise or decline in commodity prices, input costs, interest rates, weather, tourism and labor availability can all play a role in determining the market value of real estate, as outlined in more detail below.

Other land value reports, like the USDA, often rely on the recollection or thoughts of agricultural lenders reported by survey. This survey method, while useful for general market awareness, lacks the extensive research, analysis, and expertise that supports GreenStone’s benchmarking study. Additionally, by re-valuing the same property every year, GreenStone eliminates most of the inherent variance present in survey methods and is able to focus solely on market trends.

Cash Crop and Dairy

The Saginaw Valley cash crop land did not see an increase in value for 2023, after seeing a more than 16% jump in value last year. It represents a historically strong agricultural area; this surprising stagnation may be an early indication of plateauing land values to come in other agriculturally rich communities.

All other cash crop focused trends saw the anticipated increases. While other factors are present, land scarcity and competition are the primary drivers of increasing values in these areas. For instance, the property located in western northeast Wisconsin is located in the western part of GreenStone’s northeast Wisconsin territory. This area is strongly influenced by the dairy market, producers are always looking for opportunities to expand their land base. This expansion increases competition for land and thus, increases land values.

The benchmark representing a CAFO sized dairy operation saw the largest year-over-year increase in value. Our team attributes this jump to increased construction costs and a stronger dairy market than in past years.

Transitional and Recreational

Transitional land, which is typically considered agricultural land being converted to urban development, saw a small increase in Southeast Michigan as indicated in the chart. However, the same land category in Michigan’s Southern Thumb benchmark property saw a plateau. After a significant increase in recreational land value last year, the northern Michigan benchmark this year indicates things are settling down in that area, as well. Given these results, it may be plausible that the boom in rural land buying during the COVID-19 pandemic is softening as a result of increasing interest rates.

These results benefit you!

While the price to acquire land is now higher, your existing land assets are also likely worth more today than last year. That is good news for current land owners, but presents challenges for those looking to purchase land in the future. Regardless of current buying complications, history has proven that the purchase of land is a solid investment into your future.

Tracking this data annually keeps both our customers and our staff aware of where values are headed and prevents any big surprises year after year; and informs our property appraisers to help accurately value land. GreenStone’s team of lending experts are here to help you navigate the fluctuating market and find solutions for your dreams!